Popular Keywords

panel

Insights

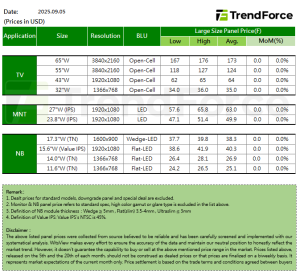

[Insights] Panel Prices in Early September: TV Expected to Hold Steady Amid Year-End Demand Prep

.TV As September begins, TV brands are preparing for year-end promotional demand, helping to sustain relatively stable momentum in panel procurement. In response, panel makers have adopted a more proactive stance in production and shipments over the past two months, easing the downward pressure...

Insights

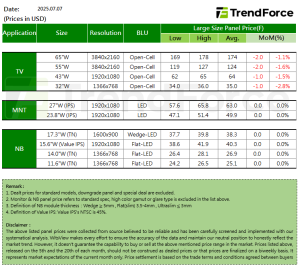

[Insights] Panel Prices in Early July: TV Panels Slightly Dip as Brands Bargain amid Weakening Demand

TrendForce discloses the latest panel prices for early July, with details as follows. TV TV panel demand remains sluggish as July begins, with some brands continuing to trim their Q3 orders to better manage inventory and gain more leverage in price negotiations with panel makers. Since Q3 st...

News

[News] Apple May Choose LGD as Second Supplier for iPhone SE 4 OLED

The iPhone SE series is Apple's budget-friendly option, traditionally sourcing screens exclusively from the Chinese manufacturer BOE. However, a report from Korean media outlet The Elec indicated that Apple is expected to use LG Display (LGD) as the second supplier for the OLED screens of next year'...

In-Depth Analyses

TV and Monitor Panel Prices Stabilize, Notebook Prices Continue to Rise in Late September

TV panel prices have reached relatively high levels after nearly two-quarters of increases. Brand customers face the dual pressures of weak demand and rising procurement costs, leading to early adjustments in their purchasing strategies. Third-quarter TV panel procurement has been revised down from ...

In-Depth Analyses

TV Panel Prices Soar in Late May, While Laptop and Monitor Panel Prices Remain Unchanged

Demand for stocking up ahead of the upcoming June 18th promotion is dwindling, and the TV panel market is gradually returning to normal levels. Panel manufacturers are carefully managing production rates to maintain a balanced supply and demand. As a result, TV panel prices are expected to continue ...

- Page 1

- 2 page(s)

- 8 result(s)