Reflecting these tightening dynamics, Samsung Electronics and SK hynix have reportedly halted or postponed DRAM price negotiations with several clients, Munhwa Ilbo notes. As memory prices surge, both companies are carefully watching market trends before finalizing supply decisions.

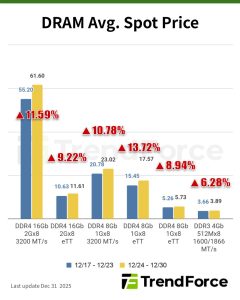

This broader uptrend in general-purpose DRAM is being reinforced by surging server DRAM demand. TrendForce’s latest investigations show that server DRAM contract prices are strengthening in 4Q25, driven by ongoing data center expansion among global CSPs. This momentum is lifting overall DRAM pricing. As a result, TrendForce has revised its 4Q25 outlook for conventional DRAM pricing upward, from an earlier forecast of 8–13% growth to 18–23%, with a strong likelihood of further upward revision.

Notably, TrendForce highlights that, with server demand remaining strong, DDR5 contract prices are expected to maintain an upward trajectory throughout 2026, particularly in the first half of the year.

Read more