Popular Keywords

About TrendForce News

TrendForce News operates independently from our research team, curating key semiconductor and tech updates to support timely, informed decisions.

[News] Taiwan DRAM Makers Reportedly Eye 20-50% Q4 Contract Price Hikes amid DDR4 Supply Squeeze

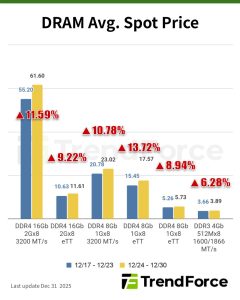

With DDR4 prices already firm on tight supply, the memory market is bracing for another rally as the electronics industry enters its seasonal peak in the second half, according to the Commercial Times. After sharp gains in Q3, contract prices are projected to rise a further 20%–50% in Q4, as Taiwanese and Korean suppliers curb output to tighten supply, the report says.

As per Commercial Times, Taiwan’s Nanya Technology raised contract prices 70% quarter over quarter in Q3 and is set for another 50% increase in Q4. Winbond, meanwhile, reportedly posted a 60% jump last quarter and is expected to add another 20% in Q4—driving contract prices 80%–90% above Q2’s trough. The report notes that both companies could return to profitability sooner than anticipated.

As memory makers accelerate their shift to DDR5 and HBM, analysts cited by the report project that by Q4 2026, global DDR4 capacity will fall to just 25%–33% of Q1 2025 levels, as Samsung, SK hynix, Micron, and China’s leading DRAM supplier phase out production.

In contrast, Taiwanese makers are moving to seize the supply gap. Nanya Technology is boosting DDR4 capacity by 50% to absorb demand left by global exits, while Winbond has added new lines to produce 8Gb DDR4, according to Commercial Times. Analysts cited by the report say the strategy could significantly expand their market share by 2026 and gradually challenge Korean dominance in the DDR4 segment.

Interestingly, while Samsung and SK hynix had planned to end DDR4 shipments between late 2025 and early 2026, they are now expected to extend production into next year amid soaring DDR4 prices, Maeil Business Newspaper reported.

TrendForce’s latest findings also reveal the DDR4 market is set to remain in a persistent state of undersupply and strong price growth through 2H25.

Notably, compared with PC and server segments, supply in the consumer DRAM market is even more constrained, as per TrendForce. This segment—covering applications such as industrial control, networking, TVs, consumer electronics, and controllers—mainly uses DDR4, which ranks behind PC and server applications in suppliers’ allocation priorities. As a result, supply-demand imbalance is particularly severe. TrendForce data shows July consumer DDR4 contract prices have already risen by more than 60–85%, leading to a sharp upward revision for 3Q25 contract prices to a quarterly increase of 85–90%.

Read more

(Photo credit: Nanya Technology)

Please note that this article cites information from Commercial Times and Maeil Business Newspaper.