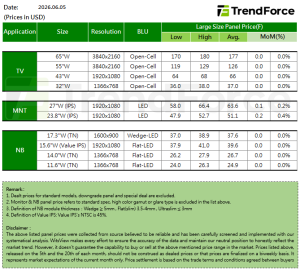

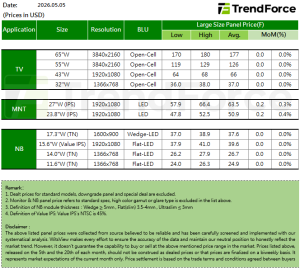

Full-size TV panel prices to rise above cash costs in May, while notebook panel prices remain stable

In May, TV panel prices are expected to continue rising due to strong inventory momentum and dynamic operating capacity utilization by panel manufacturers. Especially Chinese manufacturers aim to restore TV product profits to above break-even points by the end of Q2, so the price increase of TV panels in May is significant. Full-size TV panel prices are expected to increase by 1~10 USD, which are all predicted to rise above cash costs in May.

VA panels are in higher demand than IPS panels for monitors currently, and Open Cell panel prices have slightly risen in recent months. The monitor panels are expected to continue to rise by 0.3~0.5 USD in May. Module product demand outlook is uncertain, with limited price increase space, so prices will likely remain stable in May. Taiwanese panel manufacturers have released information on price increases for monitor panels, and their impact on the market atmosphere and price trends needs to be observed still.

Demand momentum for notebook panels is slowly increasing, but the overall demand outlook is unclear, so the NB brands remain conservative attitude on their panel inventory. Meanwhile, the NB brands are expected to be high-maintenance while dealing with the tentative messages about raising the NB panel prices from panel manufacturers. Therefore, TrendForce believes that notebook panel prices are expected to remain stable in May.