According to TrendForce research, global monitor shipments have stabilized at approximately 125–130 million units annually in the post-pandemic era. Within this landscape, OLED monitors have emerged as a standout high-growth segment since 2023, with brands racing to adopt the technology and panel makers reallocating their capacity accordingly.

OLED Monitor Shipments Continue to Scale, Penetration Rate Accelerating

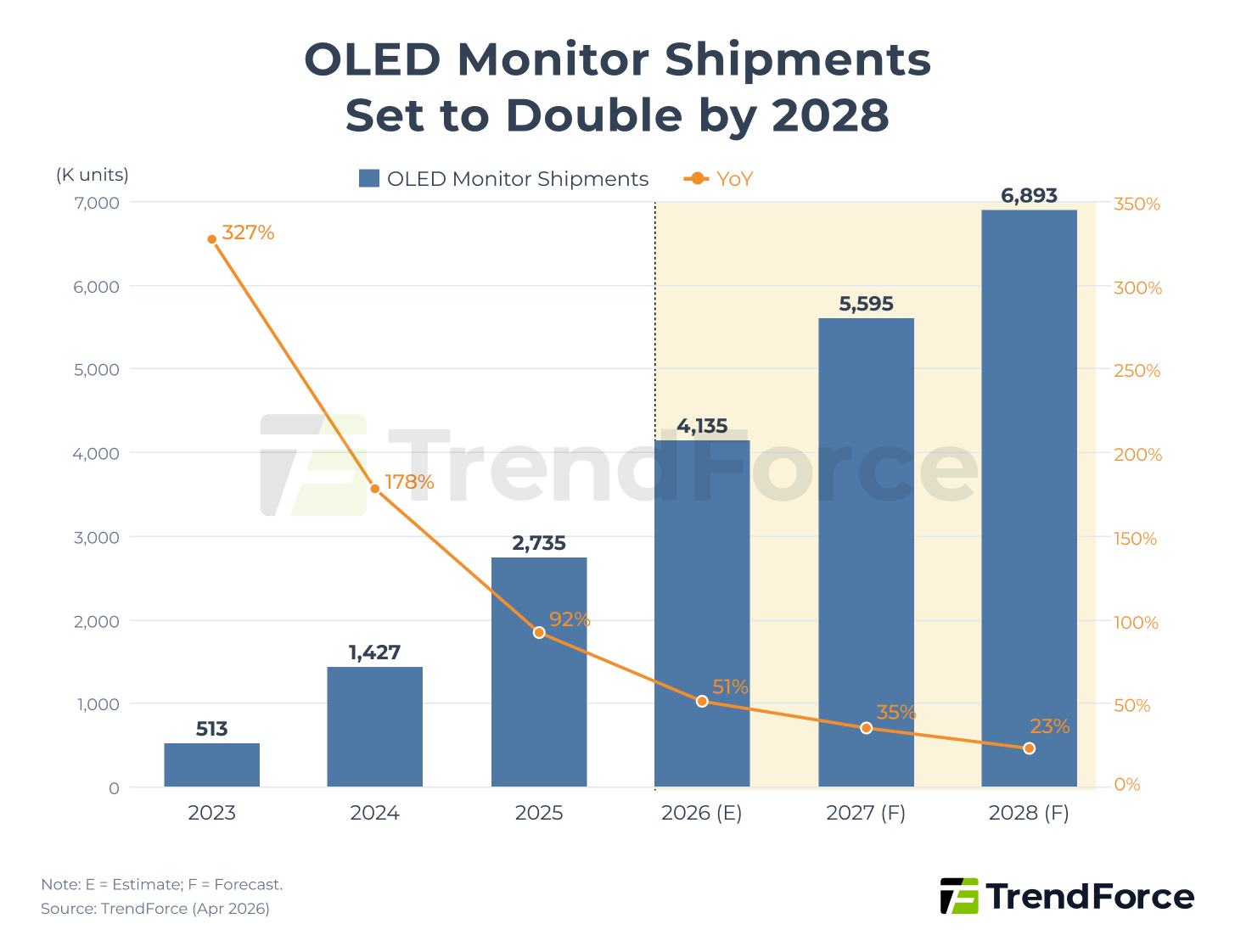

As shown in Figure 1 below, global OLED monitor shipments reached 2.735 million units in 2025, representing a staggering 92% YoY increase. TrendForce projects shipments will surpass the 4 million mark in 2026 and continue to scale to 6.893 million units by 2028. Although YoY growth will naturally moderate as the base grows, it is expected to remain above 20%, signaling that OLED technology has entered a rapid mainstream adoption phase driven by premium display demand.

Figure 1. Forecast of OLED Monitor Shipment Volume (Unit: K)

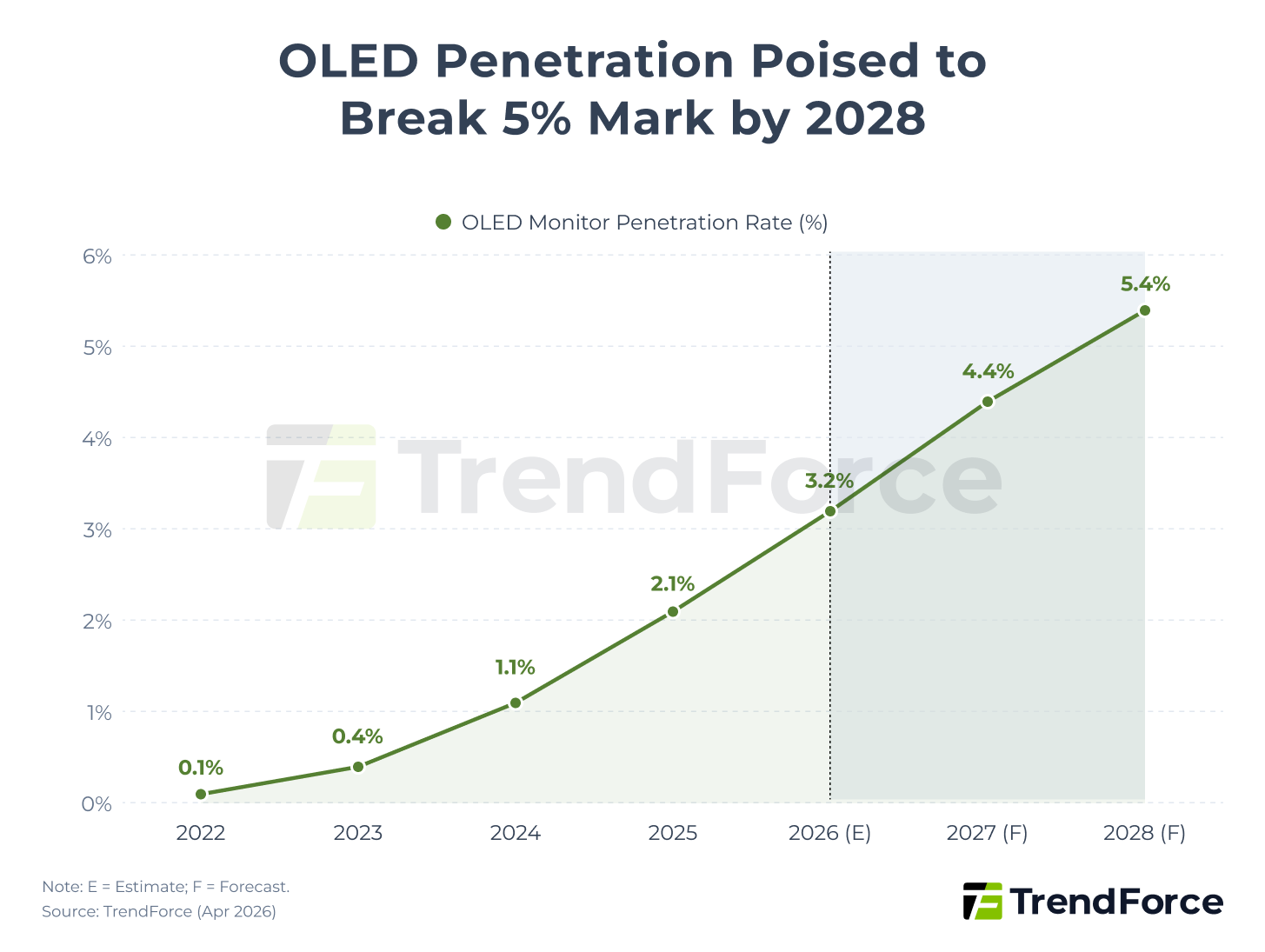

On the penetration front, OLED technology is rapidly increasing its share of the overall monitor market. Rising from just 0.1% in 2022, penetration reached 2.1% in 2025, and TrendForce forecasts it will climb further to 5.4% by 2028.

Figure 2. Forecast of OLED Monitor Penetration in the Overall Monitor Market

Brand Landscape Shifts as ASUS Claims the Top Spot, MSI Closes In

As profit margins for traditional LCD monitors continue to tighten, OLED monitors give brands new opportunities for premium market segmentation. With superior specifications and image quality, OLED monitors cater effectively to the high-end market—particularly the thriving gaming sector. This shift not only meets gamer demands but also significantly bolsters overall profitability for brand customers.

In the early years of OLED adoption, only a handful of brands were actively embracing the technology—notably Dell (Alienware) with its high-end focus, and Samsung and LG Electronics (LGE), which prioritized in-house panel utilization. Over the past two years, however, as OLED panel supply has expanded and market acceptance has grown, more brands have been scaling up their adoption. ASUS and MSI have been the most aggressive in this regard.

Both brands bring strong gaming product portfolios, and by integrating OLED panel specifications into their lineups, they have accelerated their market visibility and driven rapid shipment growth. In 2025, ASUS officially surpassed Samsung to become the top-shipping OLED monitor brand, capturing 21.6% market share, with Samsung falling to second at 19.3%.

The latest TrendForce data shows that in Q1 2026, ASUS further extended its lead to 24% market share, while Samsung held 16.4%, with shipments growing 78% YoY.

TrendForce forecasts that ASUS will retain its top position through 2026, with Samsung remaining second. MSI's shipments have risen sharply over the past few years, and the company is on track to solidify third place by 2026.

Global OLED Monitor Shipments Surged 92% in 2025 — ASUS Secures Market Leadership

Master the Market TrendsChinese and Korean OLED Panel Supply Expanding Rapidly

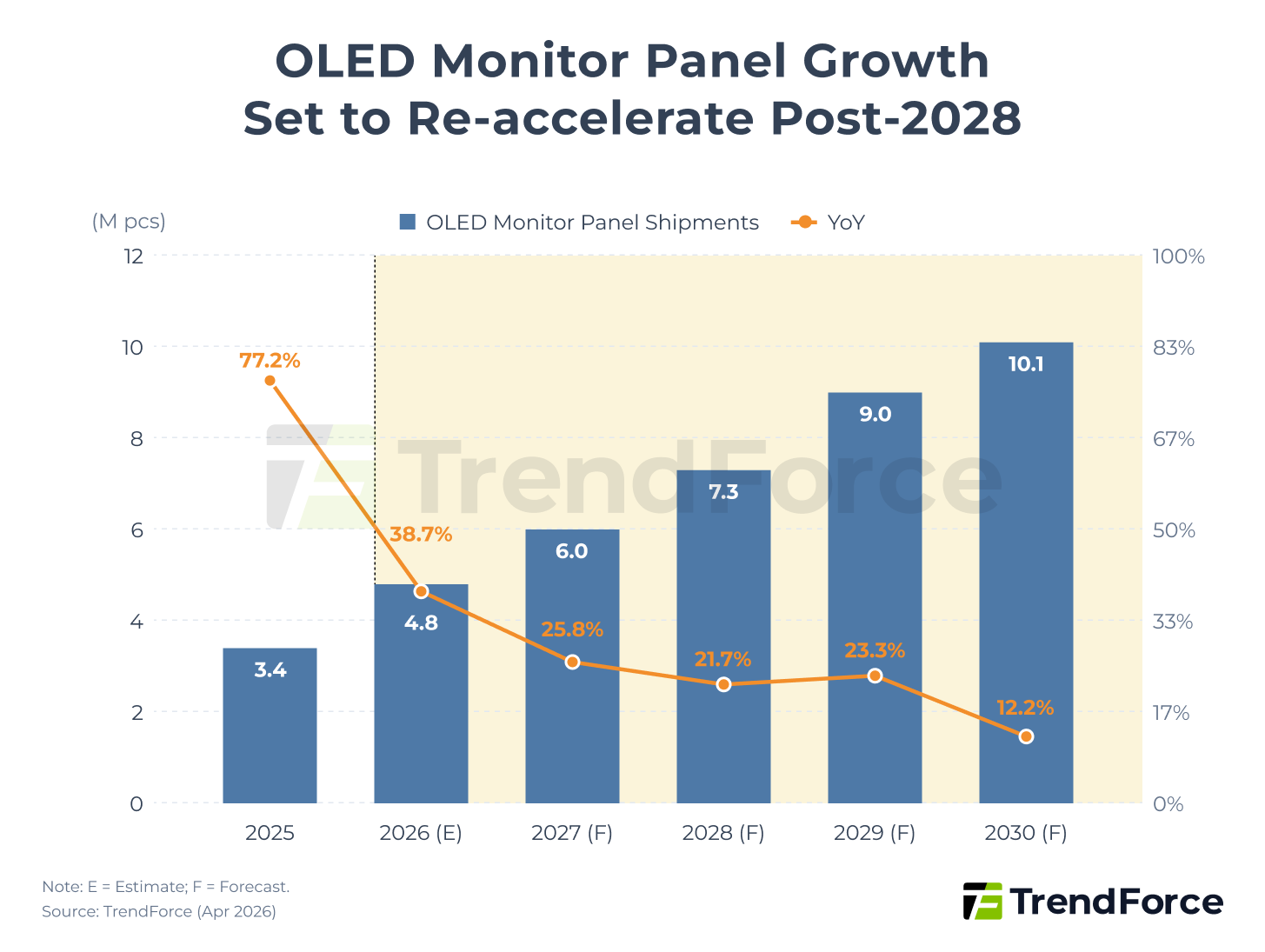

The OLED monitor panel market is in a phase of rapid growth. According to TrendForce research, OLED monitor panel shipments reached 3.3M units in 2025, up 72.2% YoY. Shipments are expected to grow to 4.7M units in 2026, representing 38.7% YoY growth. Two consecutive years of high-speed growth are primarily attributable to OLED still being in its early high-growth phase, where the low baseline significantly amplifies short-term growth rates.

Starting in 2027, the market will enter a steady expansion phase, with YoY growth expected to fluctuate within a narrow range of 25% to 32%. Looking further out, shipments are forecast to reach 10.1M units by 2030. OLED technology's penetration in the desktop monitor market continues to rise, solidifying its status as the mainstream choice in the premium segment.

Figure 3. Forecast of OLED Monitor Panel Shipment Volume (Unit: M)

Notably, the 2030 growth rate is expected to tick slightly higher to 31.6%, largely because CSOT (TCL CSOT)—a potential third major supplier beyond SDC and LGD—is expected to bring its new Gen 8.6 Inkjet-Printed (IJP) OLED line online after 2027, adding meaningful incremental volume to the global supply chain.

Korean Panel Makers Lead; CSOT Enters the Race

The two leading players in the market, Samsung Display (SDC) and LG Display (LGD), have both shifted their strategic focus heavily toward the OLED display business. SDC shipped 2.6M units in 2025, up 82.4% YoY, and has set an aggressive shipment target of 4.2M units for 2026. LGD had previously been more conservative about committing its strategic resources to OLED displays; however, as the company begins to wind down its LCD display business, it is now taking a more proactive stance on OLED. Following shipments of 0.8M units in 2025, LGD's shipment target for 2026 stands at 1.5M units.

Beyond the Korean panel makers, CSOT is actively investing in its Gen 8.6 inkjet printing (IJP) OLED production line, which is expected to ramp up mass production in Q4 2027. CSOT officially announced in May 2026 that the T8 project completed its topping-out ceremony ahead of schedule.

However, compared with Samsung Display's QD-OLED and LG Display's WOLED, CSOT's IJP OLED technology still faces several key challenges:

- Yield Rate: Production yield still lags significantly behind that of Korean panel makers.

- Material Efficiency: IJP uses polymer-based emissive materials, which are currently at a disadvantage in luminous efficiency compared with the small-molecule materials used in SDC's QD-OLED and LGD's WOLED.

- Material Supply: The supply of high-performance, soluble OLED materials suitable for IJP processes is relatively limited and must be highly compatible with the characteristics of the print heads. Higher power consumption remains an unresolved issue that will require further optimization on the materials R&D side.

Should IJP OLED material development progress smoothly, CSOT is planning an annual capacity of over 2 million units to capture share in the OLED display panel market.

Chinese Brands Broaden Procurement, Driving Demand Growth

Analyzing the sources of OLED panel demand growth in 2026 from the customer side, panel shipments stand to benefit from brands' aggressive adoption strategies. Taking leading player TPV as an example, the company has repeatedly revised its procurement plan upward, with full-year purchases expected to reach 275K units by end of 2025. Moving into 2026, TPV plans to significantly increase its share of QD-OLED in its product mix. According to market intelligence, its annual QD-OLED panel procurement target will exceed 600K units.

Beyond TPV, Innocn and HKC each plan to procure more than 300K QD-OLED panels in 2026, while Lenovo and Gigabyte continue to steadily increase their OLED panel orders.

Overall, while established customers such as ASUS, MSI, and Samsung VD are all expanding their OLED procurement, Chinese brands have undoubtedly become one of the key drivers of OLED panel demand growth this year. The OLED monitor panel market in 2026 is shaping up to show broad-based growth led by Chinese brands across multiple fronts.

As brand procurement increasingly focuses on higher-end specifications and supply-chain technology integration matures further, TrendForce expects this wave of purchasing—initiated by Chinese brand customers—to significantly drive OLED technology penetration in the mainstream gaming and professional monitor markets to new highs. As brands continue to scale up their panel purchases, this will form the foundation for sustained and stable growth in OLED panel shipments over the coming years.

Dual-Track Progress on Specifications and Cost

In terms of cost and profitability, both Korean panel makers remain in a profitable position for OLED monitor panels. Compared with OLED TV panels, OLED monitor panels offer a larger profit margin—which is precisely why both Korean suppliers continue to aggressively convert more capacity toward OLED monitor panel production, improving the overall profitability of their large-size OLED businesses.

From a specification-trend perspective, OLED monitor panel sizes are evolving. Historically, OLED monitors were concentrated in large panels with unconventional aspect ratios—such as 34", 39", and 49". Over the past two years, however, 31.5" and 27" models—sizes aligned with mainstream LCD products—have gradually been introduced, accelerating overall market expansion. TrendForce currently expects Korean panel makers to launch 24.5" products by late 2026 to early 2027, continuing the push into the mid-size segment and giving customers more options.

Over the past two years, Korean panel makers have also continued to enhance their OLED panel architectures. LGD has introduced a new four-stack structure for its WOLED panels, while SDC has proposed a five-stack structure for its QD-OLED panels—both aimed at pushing panel performance, especially peak brightness, toward and beyond the 4,000-nit level. This reflects both ongoing specification upgrades and advance preparation for entering the commercial display market, where improved panel lifetime is critical.

Beyond specification upgrades, Korean panel makers are also actively optimizing costs and, in some cases, dialing down specifications—including simplifying or removing certain components and lowering specs such as peak brightness—so that lower-cost models can reach a broader range of customer segments. As depreciation on Korean OLED production lines has largely wound down, panel makers now have greater flexibility in cost and pricing. Combined with their lower-cost product roadmaps, this creates opportunities to further expand their market influence and scale.

QD-OLED Panel Supply Release Drives 78% YoY in OLED Monitor Shipments for 1Q26

Stay UpdatedBeyond 2026: Two Key Factors That Will Determine Whether Growth Momentum Can Be Sustained

OLED monitors have undeniably been one of the major highlights of the display market over the past five years, with rapid growth momentum and strong customer acceptance. For Korean panel makers, given the challenges in promoting OLED TV panels in the high-end TV segment, directing their focus toward high-end monitor applications helps absorb capacity and improve the profitability of their OLED product lines.

Whether OLED monitors will face meaningful challenges from miniLED-based products is a medium- to long-term issue worth monitoring. In the near term, however, brand customers remain highly interested in OLED products. While some brands have begun evaluating the potential of miniLED technologies in the mid- to high-end monitor market, miniLED still finds it difficult to shake the premium image and established positioning that OLED monitors have built at the high end—and is unlikely to close the gap in market scale anytime soon.

Judging from OLED's technological maturity and current market dynamics, brand-side demand is expected to remain robust in 2026–2027, and the supply chain will continue to be dominated by the two Korean panel makers. Although new capacity is expected to inject additional momentum into the market, we remain cautious about the shipment contribution from CSOT after 2027, given existing technical bottlenecks.

Whether overall OLED monitor market growth can exceed expectations will ultimately depend on the pace of capacity expansion by Korean panel makers, and the progress of Chinese panel makers in improving yield rates and optimizing costs.

FAQ

Q1: What advantages do OLED monitors have over LCD monitors?

OLED monitors feature self-emissive pixels, delivering superior contrast ratios, faster response times, and more accurate color reproduction compared with LCD. They are currently concentrated in the mid- to high-end gaming and professional monitor segments.

Q2: What is the forecast for OLED monitor panel shipments in 2026?

According to TrendForce research, OLED monitor panel shipments in 2026 are estimated at 4.7M units, representing 38.7% YoY growth.

Q3: Which brands lead OLED monitor shipments, and who is scaling up panel procurement?

The top three OLED monitor brands by shipments are currently ASUS, Samsung, and MSI. On the panel procurement side, Chinese brands—including TPV, Innocn, HKC, and Lenovo—are significantly ramping up their purchases in 2026, making them a primary driver of demand growth.

Q4: When might CSOT enter the OLED monitor panel supply chain?

CSOT's IJP OLED Gen 8.6 production line is expected to ramp up in Q4 2027. However, the company still faces technical hurdles in yield rates, material efficiency, and supply-chain readiness, and the timeline for meaningful volume contributions remains subject to ongoing observation.

Q5: Could OLED monitors be displaced by miniLED?

Not in the near term. miniLED still struggles to replicate the brand recognition and market positioning that OLED has established at the premium end, and the majority of brand customers continue to rely on OLED as the core specification for their high-end product lines.