DRAM Market Bulletin - Jul. 8, 2026

Last Modified

2026-07-08

Update Frequency

Weekly

Format

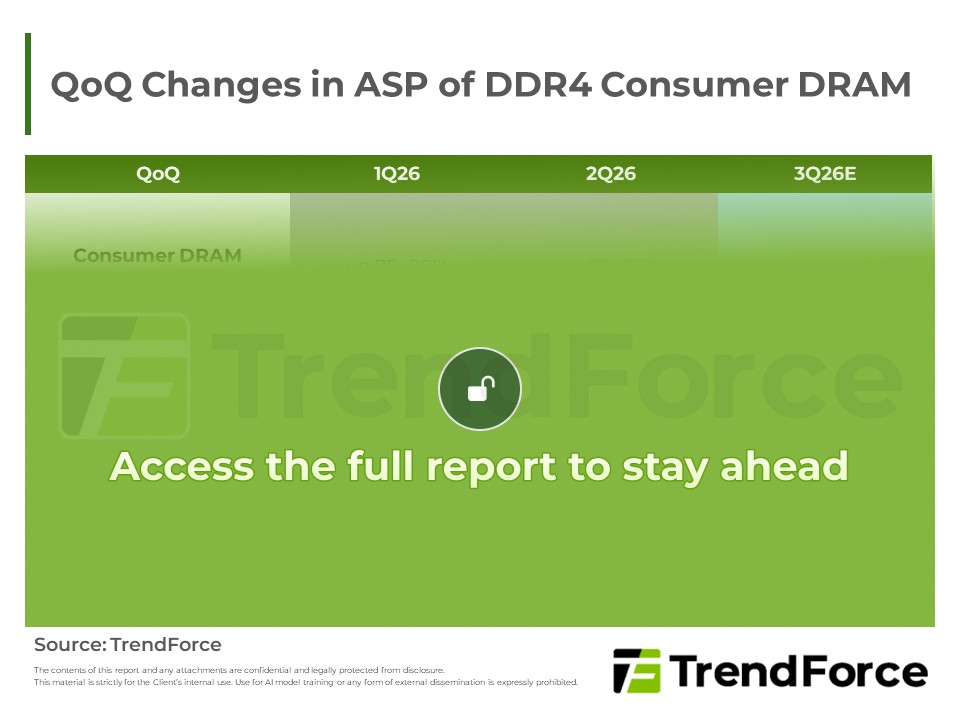

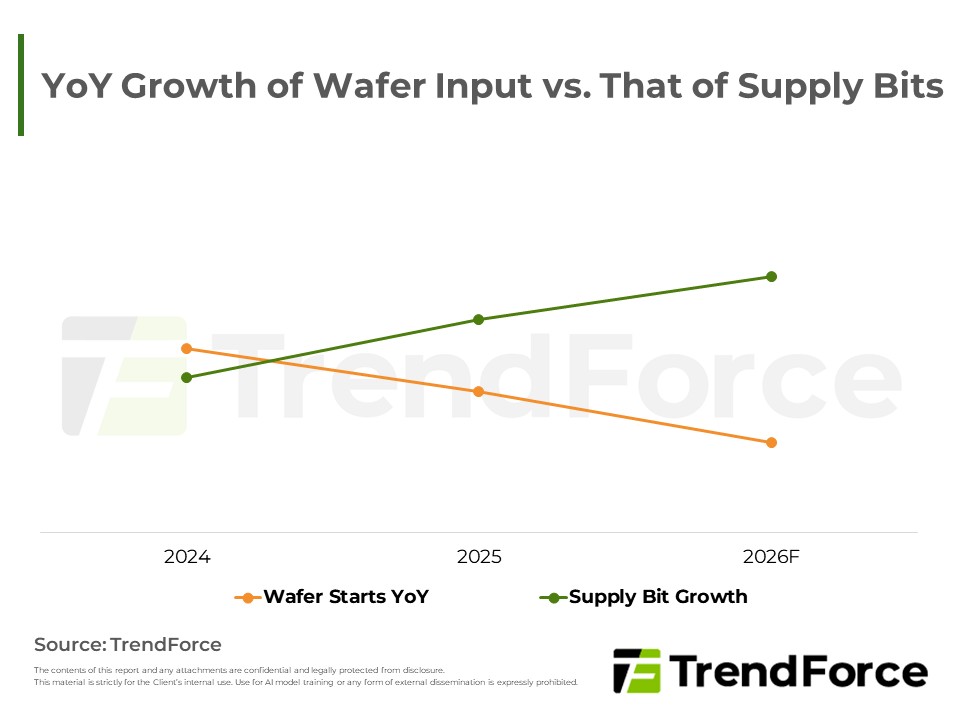

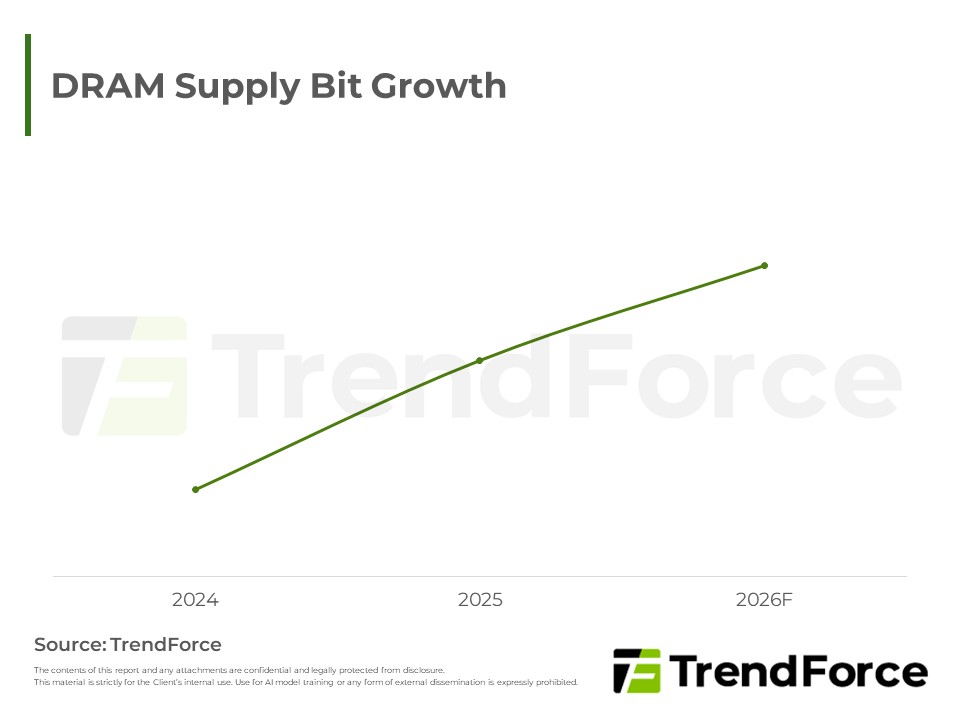

In 3Q26, top DRAM makers are prioritizing server production, severely squeezing consumer DRAM supply; consumer contract prices are set to rise well ahead of server DRAM, while PC DRAM edges only slightly higher. In 2H26, robust mid-to-high-density demand—led by AI-driven server SSDs and networking—will support consumer DRAM. Yet limited near-term capacity additions from Taiwanese makers cannot fill the gap left by the majors' exit, so the structural shortage is unlikely to ease soon.

Key Highlights

- Capacity Reallocation Reshapes Contract Pricing: With top DRAM makers prioritizing server demand, consumer DRAM supply is severely squeezed; its contract price gains are expected to significantly outpace server DRAM, while PC DRAM rises only modestly above server levels.

- Muted Spot Market: Buyers remain on the sidelines and reluctant to chase higher prices, keeping transaction volumes limited.

- Niche Applications Sustain Mid-to-High-Density Demand: Driven by AI infrastructure, shipment growth in enterprise server SSDs and networking equipment becomes the primary demand driver for consumer DRAM in 2H26, concentrated in 8Gb and 16Gb chips.

- Structural Shortage to Persist: As major suppliers accelerate their exit from mature nodes, demand shifts to Taiwanese makers. Although they are optimizing product mixes and accelerating mass production and validation of higher-density chips, new fabs remain under construction and the added output cannot fill the gap—leaving the market undersupplied for the near term.

Table of Contents

- Market Update

- TrendForce’s View

- QoQ Changes in ASP of DDR4 Consumer DRAM

<Total Pages: 2>

Category: DRAM

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

3Q26 Memory Price Forecast

2026/06/30

Semiconductors

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Semiconductors

PDF

DRAM Market BulletinRelated Reports

Download Report

8,000

Membership

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

3Q26 Memory Price Forecast

2026/06/30

Semiconductors

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Semiconductors

PDF