MLCC Market Bulletin - Jan. 9, 2026

Last Modified

2026-01-09

Update Frequency

Aperiodically

Format

Global growth is slowing under tariff and inflation pressures, while AI drives ICT but crowds out capacity and lifts costs, pushing up prices for memory, PCB and end devices, which may curb demand. Supply chains are split between fully loaded AI segments and constrained consumer products, shifting vendors’ focus from aggressive growth toward tighter risk management.

Key Highlights

- Geopolitics and tariffs drive supply‑chain relocation, keeping raw material and logistics costs elevated; AI demand lifts copper, memory, storage and PCB prices.

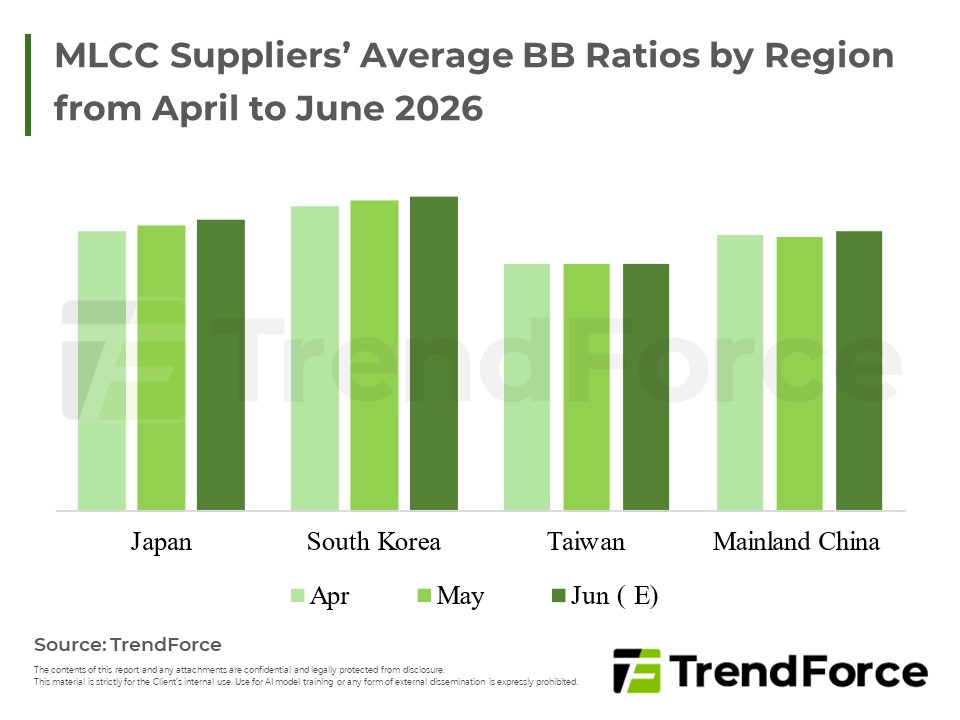

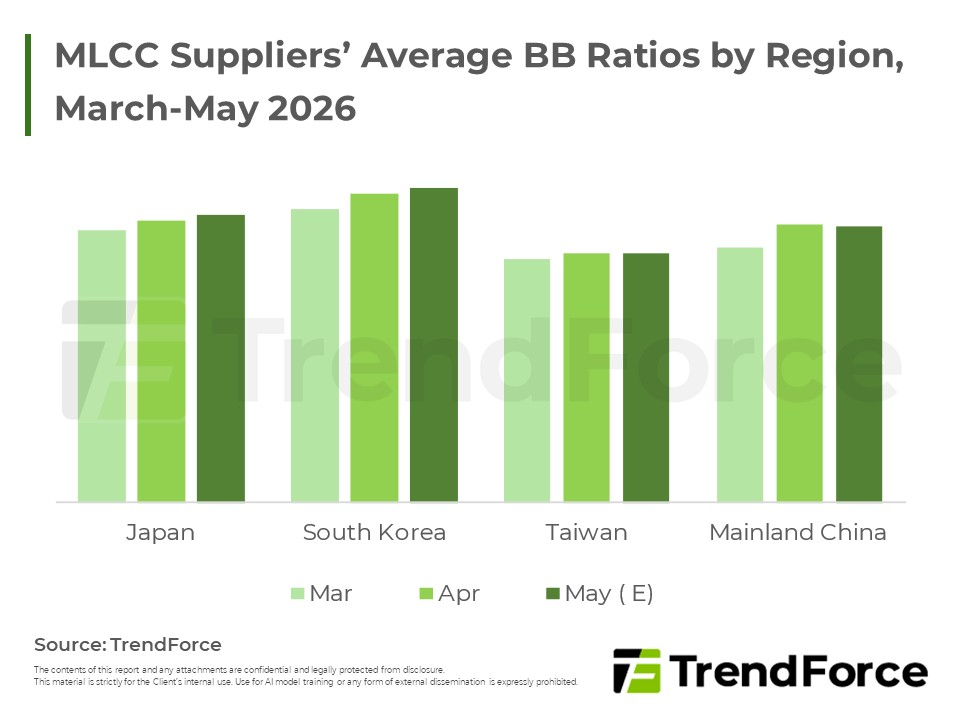

- Strong AI server orders fully load selected ODMs and high‑end MLCC lines, while notebook, handset and auto demand stays soft and inventory discipline tight.

- AI capacity crowding causes PC‑related component shortages and price hikes, forcing higher device prices and raising downside risk for end demand.

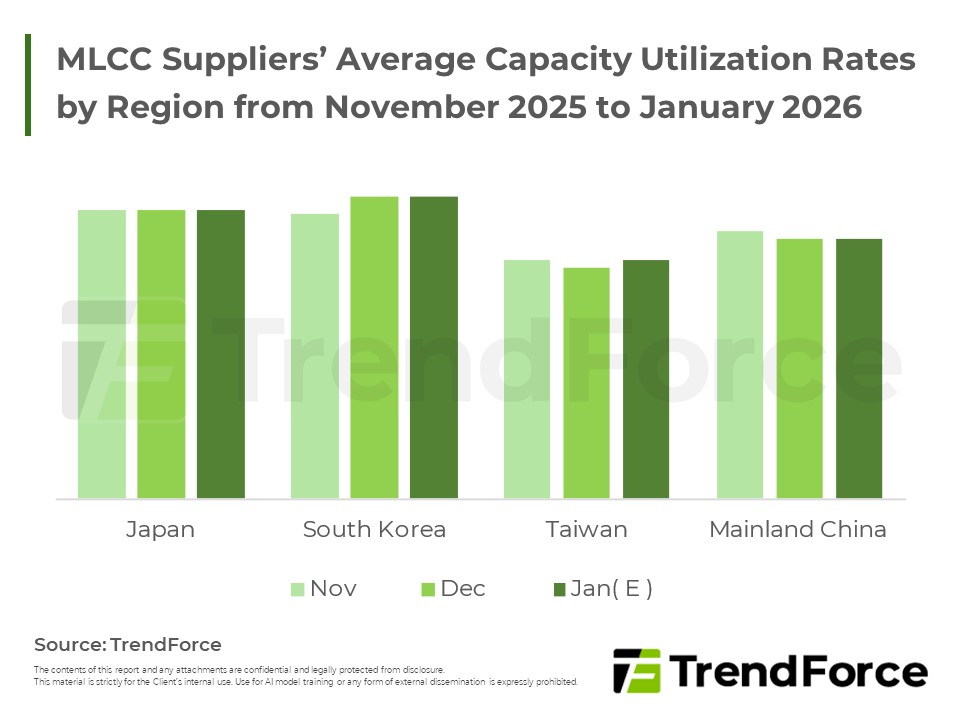

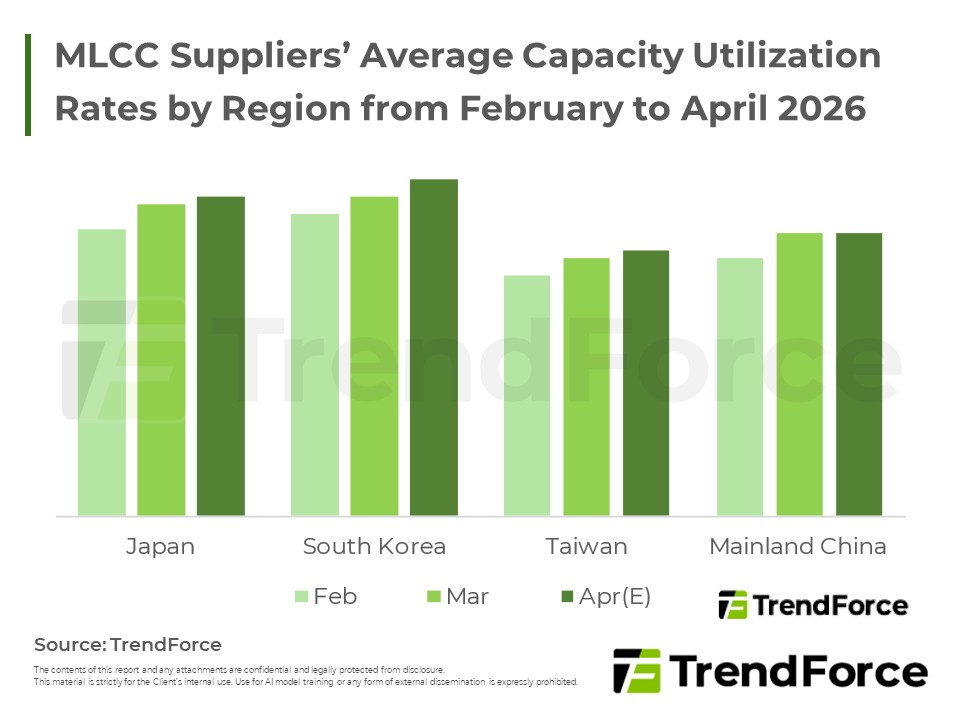

- Japanese and Korean vendors benefit from high‑end portfolios with higher utilization; Taiwan and China players lean on consumer segments and run more cautious.

- Policy uncertainty, concern over AI investment returns and tighter vertical integration heighten capital‑market scrutiny of AI expansion.

- Any slowdown in AI infrastructure could ripple from upstream chips and passives to end devices, becoming a key ICT risk.

Table of Contents

- Market Update

- Trendforce's View

<Total Pages: 4>

Category: MLCC

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Semiconductors

PDF

-

3Q26 Memory Price Forecast

2026/06/30

Semiconductors

PDF

MLCC Market BulletinRelated Reports

Download Report

4,500

Membership

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Semiconductors

PDF

-

3Q26 Memory Price Forecast

2026/06/30

Semiconductors

PDF