2Q25 Revenue Ranking among Enterprise SSD Suppliers

Last Modified

2025-08-27

Update Frequency

Quarterly

Format

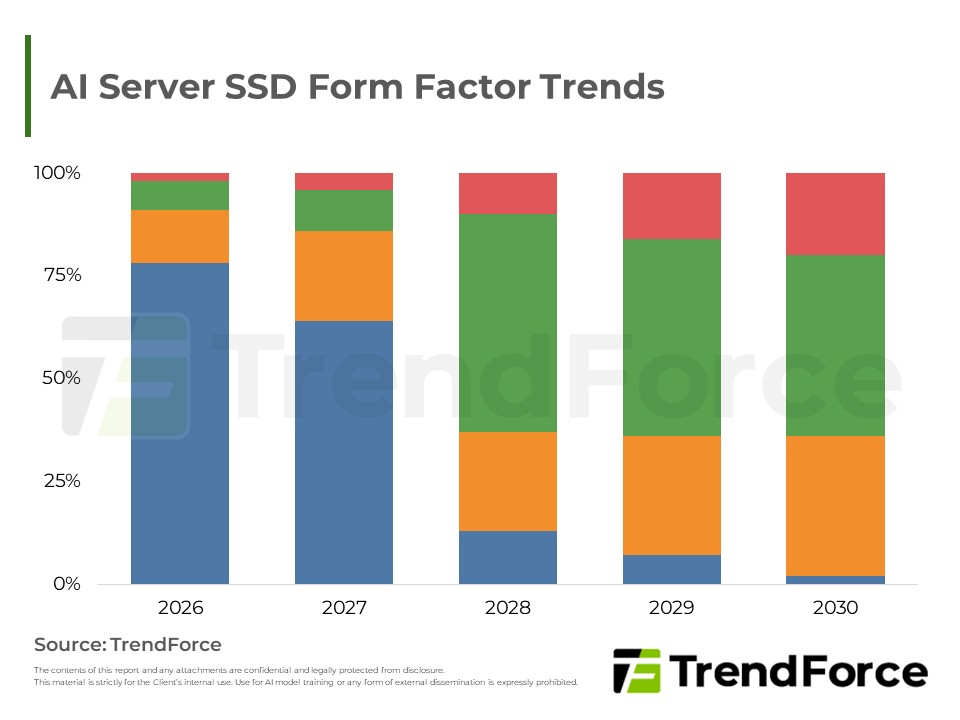

The 2Q25 Enterprise SSD market experienced significant growth, driven by robust AI applications and expanding general server deployments. However, severe supply chain challenges, including DDR4 memory and controller IC substrate shortages, led to widespread supply shortfalls. Future competition will center on advanced technology adoption like PCIe 6.0 and higher NAND Flash densities, the accelerating localization trend in China, and persistent supply-demand imbalances. Suppliers must master precise capacity planning and technological upgrades to navigate rising technical thresholds and geopolitical dynamics. Major players are strategically positioning themselves to consolidate or expand market share.

Key Highlights

- 2Q25 Market Overview:

- Enterprise SSD demand saw substantial growth, fueled by AI applications and expanded general server deployments.

- Key drivers included NVIDIA's Blackwell platform rollout and increased general server build-outs by North American CSPs.

- Supply chain faced severe constraints from DDR4 memory and controller IC substrate shortages, leading to widespread supply shortfalls.

- This imbalance resulted in varied revenue performance and market share shifts among suppliers.

- Future Trends & Challenges:

- AI-Driven Technology Iteration: Rapid adoption of PCIe 6.0 SSDs and higher NAND Flash densities (2XXL+) will raise technical and investment barriers, demanding agile capacity adjustment and technology upgrades from suppliers.

- China Market Dynamics: The accelerated "localization" trend, with the rise of YMTC and domestic controller IC vendors, will increasingly impact international players' order momentum in China.

- Persistent Supply Chain Imbalance: Managing diverse old and new production capacities amidst rapid technological evolution will make supply-demand equilibrium a continuous challenge.

- Key Supplier Strategies:

- Samsung: Maintained market leadership by absorbing urgent orders and avoiding DDR4 impact; focusing on PCIe 6.0 and 286L technology while navigating increased competition from China and client self-developed SSDs.

- SK Group: Achieved the strongest growth through high-capacity SSD demand and key North American CSP partnerships; strategically targeting HDD replacement with Nearline QLC Enterprise SSDs for Inference AI applications.

- Micron: Strategically abandoned UFS 5.0 controller IC development to fully invest in higher-margin Enterprise SSDs; aims to be an AI-era "one-stop solution" provider across HBM, server DRAM, and Enterprise SSD.

- Kioxia: Leveraging its leading Hybrid Bonding technology for high-speed AI applications; collaborating with CSP clients and third-party controller vendors to capitalize on the trend of self-developed SSDs.

- SanDisk: Actively developing next-generation products for Inference AI, including HBF technology (with SK hynix partnership), Ultra QLC, and Nearline QLC SSDs; accelerating collaborations with third-party controller IC providers.

Table of Contents

- Enterprise SSD Revenue Rose by Nearly 15% QoQ for 2Q25 as AI Applications and General Server Deployments Drive SSD Demand

- Future Trends and Challenges: Navigating Technological and Geopolitical Dynamics

- 2Q25 Revenue Ranking among Enterprise SSD Suppliers

<Total Pages: 6>

Category: NAND Flash , AI/HBM/Server

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

2Q26 Memory Price Forecast

2026/03/26

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

DRAM Contract Price Mar. 2026

2026/03/31

Semiconductors

PDF

Enterprise SSD PackageRelated Reports

Download Report

25,000

Membership

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

2Q26 Memory Price Forecast

2026/03/26

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

DRAM Contract Price Mar. 2026

2026/03/31

Semiconductors

PDF