DRAM Market Bulletin - Jul. 30, 2025

Last Modified

2025-07-30

Update Frequency

Weekly

Format

Contract pricing undecided; DDR4/LPDDR4x see stronger increases. DDR4 spot trading outpaces DDR5, with DDR5 prices declining. SK hynix benefits from AI and tariffs, DDR4 drives inventory down. HBM market competition and next-gen pricing dynamics will shape future price trends and supply-demand.

Key Highlights

- Contract Market: Contract prices to be finalized in August; DDR4/LPDDR4x show stronger gains than DDR5.

- Spot Market: DDR4 trading remains active but demand eases; DDR5 prices continue softening, signaling upcoming contract price trend.

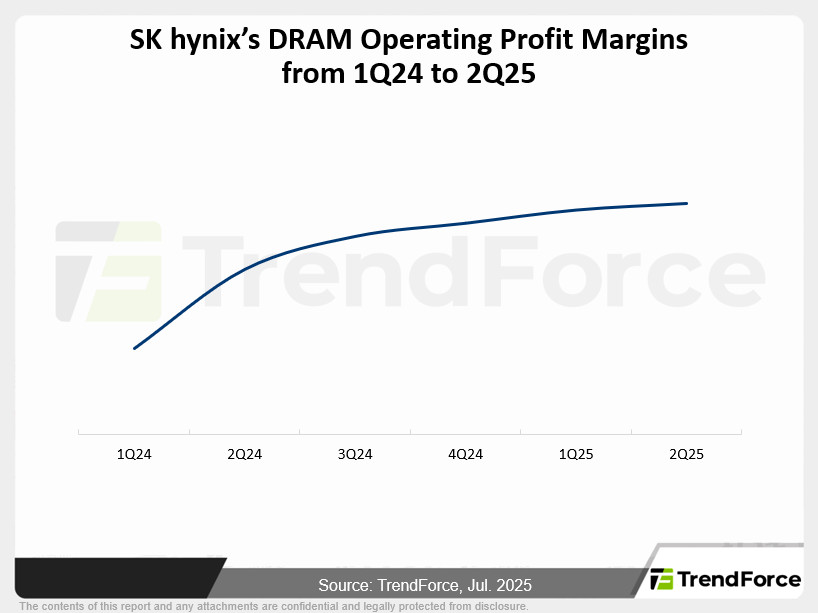

- SK hynix Results: 2Q25 shipments driven by AI/tariff demand, strong DDR4 momentum, and inventory reduction.

- Outlook: 3Q25 demand stable, OEM inventory low, DDR4 supply to become selective; EOL process progressing.

- HBM Market: 2Q25 HBM3e shipments as planned; 2026 HBM contracts still under negotiation, HBM4 pricing targets healthy profitability rather than excess premiums.

- Industry Trend: Server DDR5 inventory pressure rising; potential DRAM price decline ahead. Samsung HBM certification progress supports future average price; TrendForce will keep tracking demand-supply and price movements.

Table of Contents

- Market Update

- TrendForce's View

- SK hynix's DRAM Operating Profit Margins from 1Q24 to 2Q25

<Total Pages: 3>

Category: DRAM

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jul. 2026

2026/07/15

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

3Q26 Memory Price Forecast

2026/06/30

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Semiconductors

PDF

DRAM Market BulletinRelated Reports

Download Report

8,000

Membership

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jul. 2026

2026/07/15

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

3Q26 Memory Price Forecast

2026/06/30

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Semiconductors

PDF