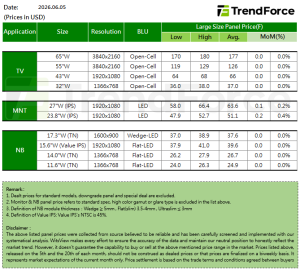

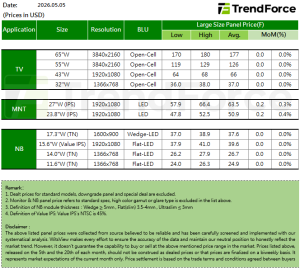

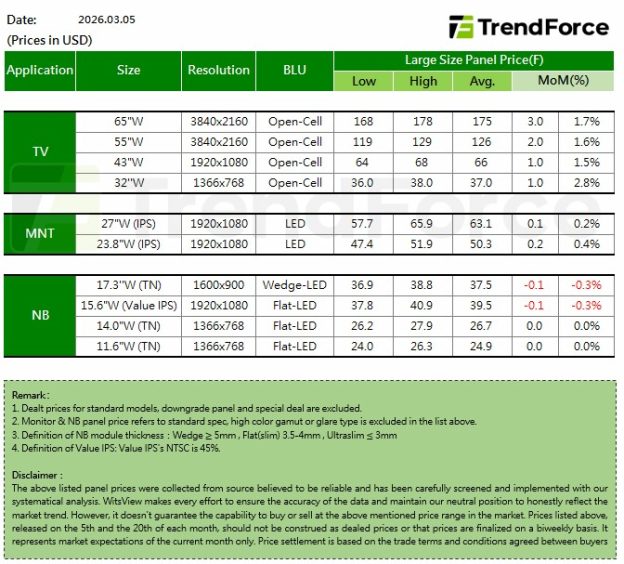

[Insights] Early March Panel Prices: TV Strength Continues; MNT Turns Up While NB Weakness Moderates

.TV

Entering March, TV demand has remained stable. North American distributors have recently agreed to raise retail prices for small- and mid-sized TVs starting in the second quarter, boosting TV brands’ confidence to increase panel procurement. With demand holding steady, panel makers are also aiming to sustain the upward momentum in TV panel prices. In March, prices are expected to rise by $1 for 32-, 43-, and 50-inch panels, $2 for 55-inch panels, and $3 for 65- and 75-inch panels.

.MNT

In March, demand for MNT panels has remained stable. Coupled with the continued rise in TV panel prices, panel makers have become more confident about raising MNT panel prices across the board. Based on current observations of mainstream MNT panel price trends in March, Open Cell panels are expected to see price increases as tight supply–demand conditions persist for 23.8-inch FHD IPS, which is projected to rise by $0.3, while 23.8-inch FHD VA is expected to increase by $0.1. 27-inch FHD IPS panels are projected to rise by $0.2. For panel modules, 23.8-inch FHD panels are also facing relatively tight supply, with prices estimated to increase by $0.2, while 27-inch FHD modules are expected to rise by $0.1.

.NB

Entering March, brand customers had stocked up more aggressively than expected in the previous two months, while panel makers had also made notable price concessions. As a result, although demand in March has remained at a relatively solid level, panel makers appear to be slightly scaling back their visible price concessions, with some discounts potentially shifting off the table. Based on current observations of NB panel price trends in March, the decline has slowed somewhat: TN models are expected to remain flat, while IPS models are projected to fall by $0.1.