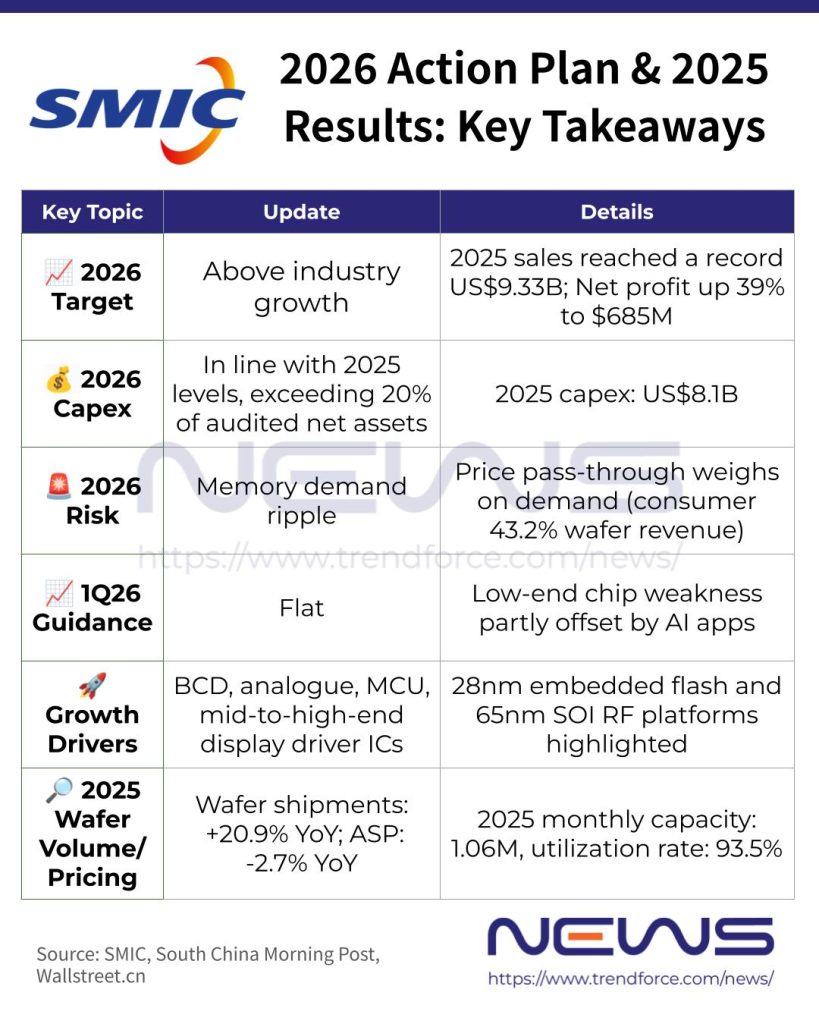

[News] SMIC 2026 Action Plan Points to Above-Industry Growth, Capex Held in Line with 2025

Amid a broader wave of price increases spreading from upstream foundries to downstream memory and analog chips, China’s leading foundry SMIC has released its 2026 action plan alongside its 2025 annual report. According to South China Morning Post, the company is targeting 2026 sales growth above the industry average under the new plan.

Wallstreetcn adds that SMIC’s capital expenditure is expected to remain broadly in line with 2025 levels, while still exceeding 20% of audited net assets. Key takeaways on its market outlook, risks and focus areas are as follows:

SMIC Warns of Memory Demand Ripple Risks

For potential risks, SMIC warned that surging AI-driven demand for memory chips is tightening supply for other consumer electronics segments such as smartphones, with price pass-through effects that could weigh on end-demand. The impact could be significant: according to Wallstreet.cn, consumer electronics accounted for 43.2% of its wafer sales in 2025, up from 37.8%, making it the company’s largest end-use segment.

Meanwhile, SMIC’s revenue base remains heavily concentrated in China amid the country’s push for chip self-sufficiency. According to Wallstreet.cn, China accounted for 85.6% of SMIC’s total revenue in 2025, up from 84.6% a year earlier, underscoring the ongoing trend of localisation and import substitution.

At the same time, SMIC continued to expand capacity amid strong domestic demand. In 2025, its monthly production capacity reached 1.06 million wafers, up by 111,000 wafers from a year earlier, according to South China Morning Post.

Process/ Research Focuses

Notably, SMIC said in its action plan that it will continue to deepen its capabilities in BCD, analogue, MCUs and mid-to-high-end display driver ICs, strengthening its position in these niche segments as it aims to achieve sales growth above the industry average in 2026.

SMIC also highlighted its progress across platforms including 28nm embedded flash and 65nm silicon-on-insulator RF processes, adding that it had accumulated 14,511 granted patents by the end of 2025, including 12,621 invention patents.

Wallstreet.cn reports that its R&D spending rose to US$774 million in 2025, though the R&D-to-revenue ratio eased to 8.3% from 9.5% a year earlier, mainly reflecting a larger revenue base.

As previously reported by Security Times, citing SMIC Co-CEO Zhao Haijun, SMIC’s 2025 capex hit $8.1 billion—above early-year guidance—fueled by strong customer demand, shifting market conditions, and extended equipment lead times. Capex for 2026 is expected to stay roughly flat.

2025 Performance Recap

The Chinese foundry giant closed 2025 on a strong note, with annual revenue reaching US$9.327 billion, surpassing 2022’s US$7.273 billion to hit a new record high. Growth was primarily volume-driven, as wafer shipments rose 20.9% year-on-year, while average selling prices edged down from US$933 to US$907 per wafer.

Net profit attributable to shareholders of the parent company reached US$685 million, an increase of 39.0% year-on-year. Despite a significant rise in depreciation, gross margin improved to 21%, up 3 percentage points from a year earlier, as noted by Wallstreet.cn.

However, SMIC’s Q1 guidance in February’s earnings call remained cautious, with the company projecting flat revenue, noting that weakness in low-end chip demand would be partly offset by strong momentum in AI-related applications. Whether SMIC can deliver growth above the industry average as outlined in its annual report remains a key focus for the market.

Read more

- [News] China Reportedly Aims to Boost 7nm, 5nm Output Fivefold in Two Years, Driven by SMIC, Hua Hong

Edit | - [News] SMIC Posts Record $9.3B in 2025 Sales; 7nm Yields Reportedly Weigh on Margins

(Photo credit: SMIC)