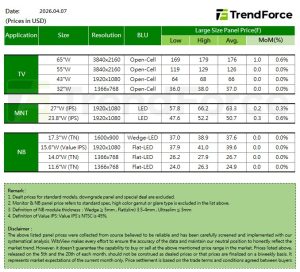

OLED TV Panel Shipments Performed Well in 2021, Korean Panel Manufacturers Completely Dominating Supply

Continued oversupply in the LCD display industry has led to a decline in the YoY profitability of panel manufacturers. As one of the key countries leading the technological development of the global display industry, Korean panel manufacturers took the lead in announcing a cutback in LCD TV products and a transition to OLED distribution.

The capacity of OLED large generational fabs building gradually, market share seized through slight price reductions

In 2021, the production capacity of LG Display’s Gen8.5 line in Guangzhou and Paju, South Korea continued to climb, obviously contributing to an increase in shipments. In addition, as OLED pricing dipped and LCD pricing advanced, the price gap between OLED TV panels and LCD panels diminished to a multiple of 2.5 in January, with the differential narrowing to a multiple of 1.8 by the middle of the year. In addition to the dwindling price divergence, OLED TVs are positioned as high-specification products, priced higher than ordinary LCD TVs at retail. After the contraction in profits posted by LCD brands, these companies delved industriously into the OLED market, driving growth in annual shipments of OLED TV up as much as 70.8% to 8.0 million units.

Supply completely dominated by Korean panel manufacturers, the trend will change in 2024 at the earliest

As an industry leader, LG Display officially began mass production of white OLED TV panels in 2017. LG Display’s hold on the exclusive supply of OLED products was broken after Samsung Display officially mass-produced QD OLED TV panels at the end of 2021. However, due to differing technologies, LG remains an exclusive supplier in the realm of white OLED TV panels.

In terms of Taiwanese manufacturers, AUO and Innolux have focused on the rollout of Mini and Micro LED panels but have not put much effort into large generational fabs for OLED panels. Japanese panel makers Sharp Display & SPDG likewise have not given OLEDs much thought. In terms of Chinese panel makers, although these companies are actively building small and medium generational fabs for OLED panels, the rollout of large generational fabs for OLED panels is still relatively slow. Therefore, the entire market structure may need to wait until 2024, when TCL’s T8 Gen8.5 inkjet OLED production line hits heavy volume before there is a chance to see any changes. However, according to the capacity observation currently planned by TCL, overall supply will be quite limited in the initial stages. Although HKC’s Changsha plant has a planned production capacity corresponding to a large generational fab for OLED panels, there is no clear plan for a specific mass-production timeframe. Thus, TrendForce expects that Korean panel makers will remain the vanguard of the trend towards OLED TV panels in the next 3 to 4 years.

(Image credit: Unsplash)