LCD TV Panel Pricing Falls to New Lows, Panel Factories Must Reduce Production

According to TrendForce, based on the quarterly supply-demand ratio, the difference in supply and demand in 1Q22 rose by 4.9% to 8.9% compared with 4Q22, much higher than supply and demand equilibrium at 5%. However, since panel makers still had room to build up inventories and IT panel pricing was still at a profitable level when at equilibrium, there remained an upside to panel makers’ overall operating interest, so there was no operation adjustment at the time.

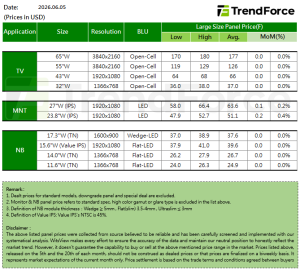

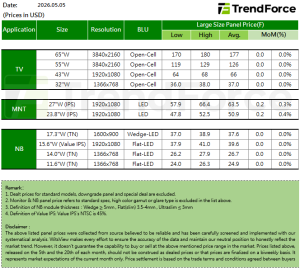

Whether TV panel demand or IT panel demand, the magnitude of corrections began to intensify in 2Q22. Since the production capacity of panel manufacturers continues trending towards growth, the supply-demand ratio is expected to widen to 11.8% and the severity of the imbalance is set to return to 2008 financial crisis levels. As TVs account for nearly 70-80% of LCD production capacity, LCD TV panel quotations have again dropped, falling to record lows. For example, 32-inch HD quotations have fallen to US$28 and 43-inch FHDs have fallen to US$55.

In light of this situation, panel manufacturers have begun looking for solutions. Other than reducing the cost of upstream materials, the most effective way to buoy pricing is to control output, so news of production cuts began to appear in 2Q22. According to research from TRI, in 2Q22, the LCD glass output area of panel makers’ large generational fabs fell by 3.3% compared with their original planning. At the same time, due to Samsung’s announcement of progressively strict procurement control, TV panel shipments are expected to be downgraded by 1.2% compared with original planning. Therefore, the supply-demand ratio will not change much as panel makers reduce production in an insignificant manner.

No peak in peak season, production reduction in 3Q22 set in stone, stocking momentum expected to pick up in 4Q22

Moving into July 2022, in the past, Q3 was traditionally the time for panel stocking. Originally, panel manufacturers expected the seasonal effect to stabilize or even produce a slight rebound in TV panel prices but the market did not react as positively as panel manufacturers believed. The world’s largest TV brand Samsung once again revised its TV panel purchases downward in 3Q22 from its original plan of 14 million units to 8-8.5 million units. Rumors that purchase volume was even less than 8 million units cannot be ruled out, again pressuring TV panel quotations which were already under pressure to keep from selling at a loss. This news can be considered the straw that broke the market’s back.

If production is not reduced, the supply-demand ratio in 3Q22 will remain on par with the ratio before production cuts in 2Q22 (11.8%). It is conceivable that if inventory from 2Q22 added, panel makers will not only face the risk of an inventory explosion, but also if the price drops again, it cannot be ruled out that all panel sizes will ship at a loss in 3Q22 because pricing has gradually approached Bom Cost. Therefore, some panel makers have begun to plan a large-scale reduction in capacity utilization in 3Q22.

HKC, CSOT, AUO, and Sharp, who count Samsung as their primary customer, are among the panel factories that will see a significant reduction in capacity utilization in 3Q22. Huike, CSOT, and AUO have all planned to greatly reduce production by 32%, 20%, and 25%, respectively, compared with their original plans for their factory campuses. Considering the high cost of its Japanese factory, Sharp needs to maintain a high utilization rate. The company only adjusted Guangzhou Gen10.5, with overall utilization rate expected at only 70-75%.

As the LCD industry bellwether, BOE is facing external resistance. Currently, there are no plans to significantly reduce the capacity utilization rate of its entire production line, with utilization adjustment only planned for the Fuqing (B10) Gen8.5, Chengdu (B19) Gen8.6+, and Hefei (B9) Gen10.5 factory campuses. Overall impact is expected to be 10-15%. CHOT plans to reduce its capacity utilization rate by 10-15% in 3Q22 compared with their original plans due to accumulating more than a month of inventory of their main product, 50-inch TV panels.

If panel makers really control production as suggested by rumors, the supply-demand ratio will have a chance to move to 6.4% in 3Q22. Although a point close to equilibrium cannot be achieved immediately, effective output control will prevent the market from deteriorating further and facilitate advantageous price movement to mitigate or even stabilize the downtrend.

If panel makers continue to control capacity utilization in 4Q22, the price of LCD TV panels is expected to fall into a sweet spot, international brands are expected to perform purchase volume adjustments in Q2 and early spring in 2023, and Chinese brands will also stock up ahead of schedule in 4Q22. Market conditions are expected to have a chance to improve in 4Q22, with a good start for 2023. Otherwise, market conditions will deteriorate again in 4Q22, which will not only cast a shadow on the beginning of 2023, but may also force some panel makes to shut down certain factory campuses due to unbearable losses.

(Image credit: Pixabay)