As the traditional TFT-LCD industry matures, Taiwanese and Korean manufacturers have strategically exited the market, leaving Chinese firms to secure dominance. However, the competitive landscape has shifted toward a newer frontier: AMOLED panels.

AMOLED (Active-Matrix Organic Light-Emitting Diode) is a high-end evolution of OLED technology. By utilizing TFT backplanes for precise pixel control, AMOLED has become the standard for premium displays. Its self-emissive nature eliminates backlight modules, enabling ultra-thin and flexible designs. This technological shift is the primary catalyst for Apple’s full transition to AMOLED, which in turn has ignited a Gen 8.6 "arms race" between China and South Korea.

Korean giants like Samsung have long dominated the AMOLED market, leveraging first-mover advantages across applications from wearables to high-end TVs. However, over the past eight years, Chinese manufacturers have aggressively expanded Gen 6 capacity to match the rise of domestic smartphone brands. The development gap between China and South Korea has narrowed significantly; as the smartphone market saturates, this rivalry is spilling over into the more advanced Gen 8.6 sector.

TrendForce observes that Taiwanese and Japanese manufacturers are losing momentum in the small-to-medium AMOLED space. As development moves toward larger generations and next-gen technologies, the massive capital requirements will serve as a high barrier to entry. The industry is poised to become a "China-Korean duopoly," defined by a high-stakes standoff between these two powers.

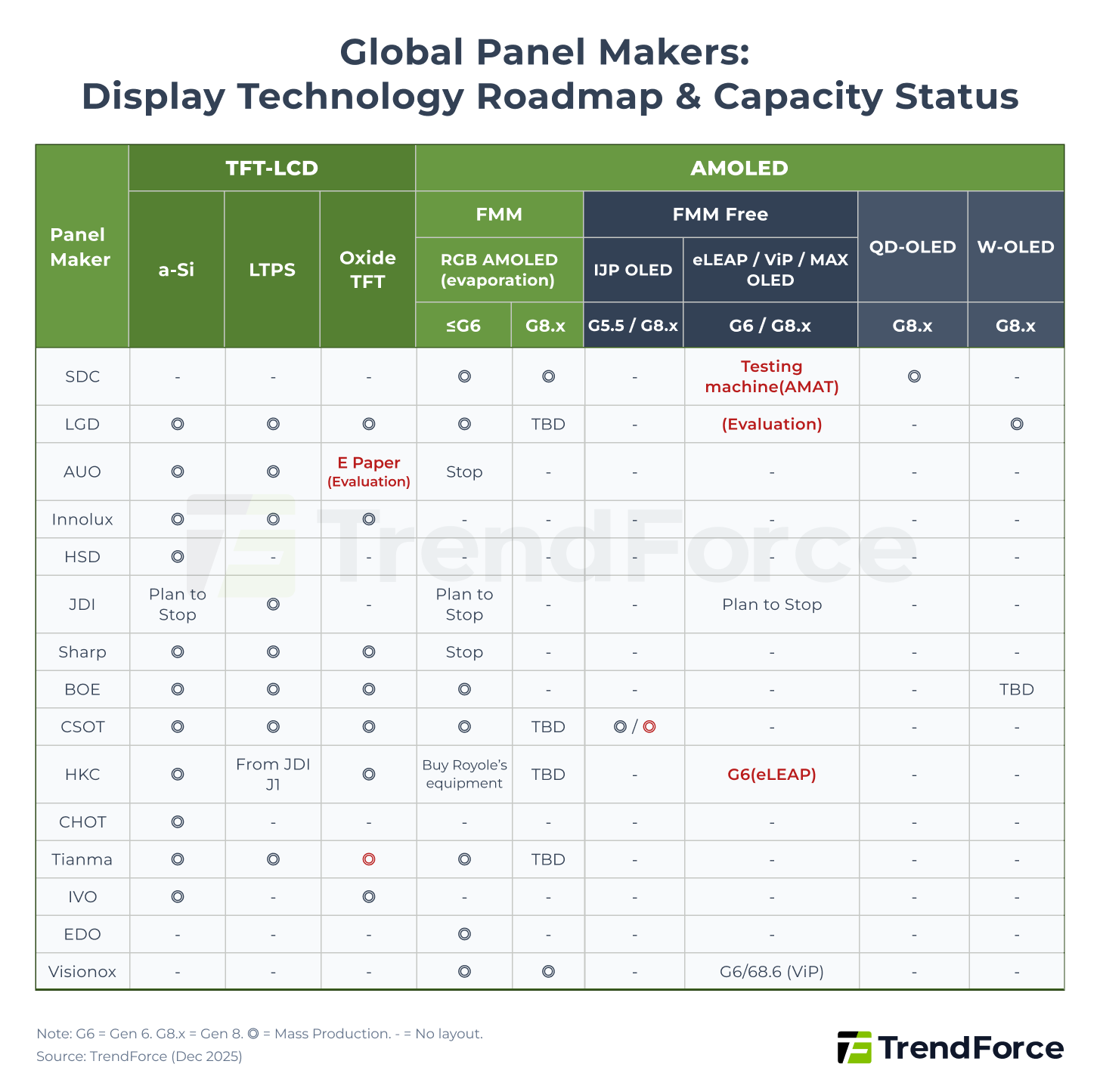

Figure 1. Global Panel Makers: Display Technology Roadmap & Capacity Status

AMOLED Panel Cost Breakdown - 1Q26

Comprehensive tracking of AMOLED cash cost structures across NB, MNT, TV, and Automotive markets. Evaluate profitability margins and competitive benchmarks through in-depth comparisons of WOLED, QD-OLED, and Tandem technologies.

Stay UpdatedApple Demand Sparks a New Wave of AMOLED Investment

Although Samsung pioneered the use of AMOLED panels in smartphones around 2010, the true industry turning point came in 2017 when Apple launched the iPhone X, its first model to feature the technology. This move officially ignited market demand, driving AMOLED penetration to surge in the following years and ultimately surpass the 60% threshold in 2025, solidifying its status as the mainstream smartphone specification.

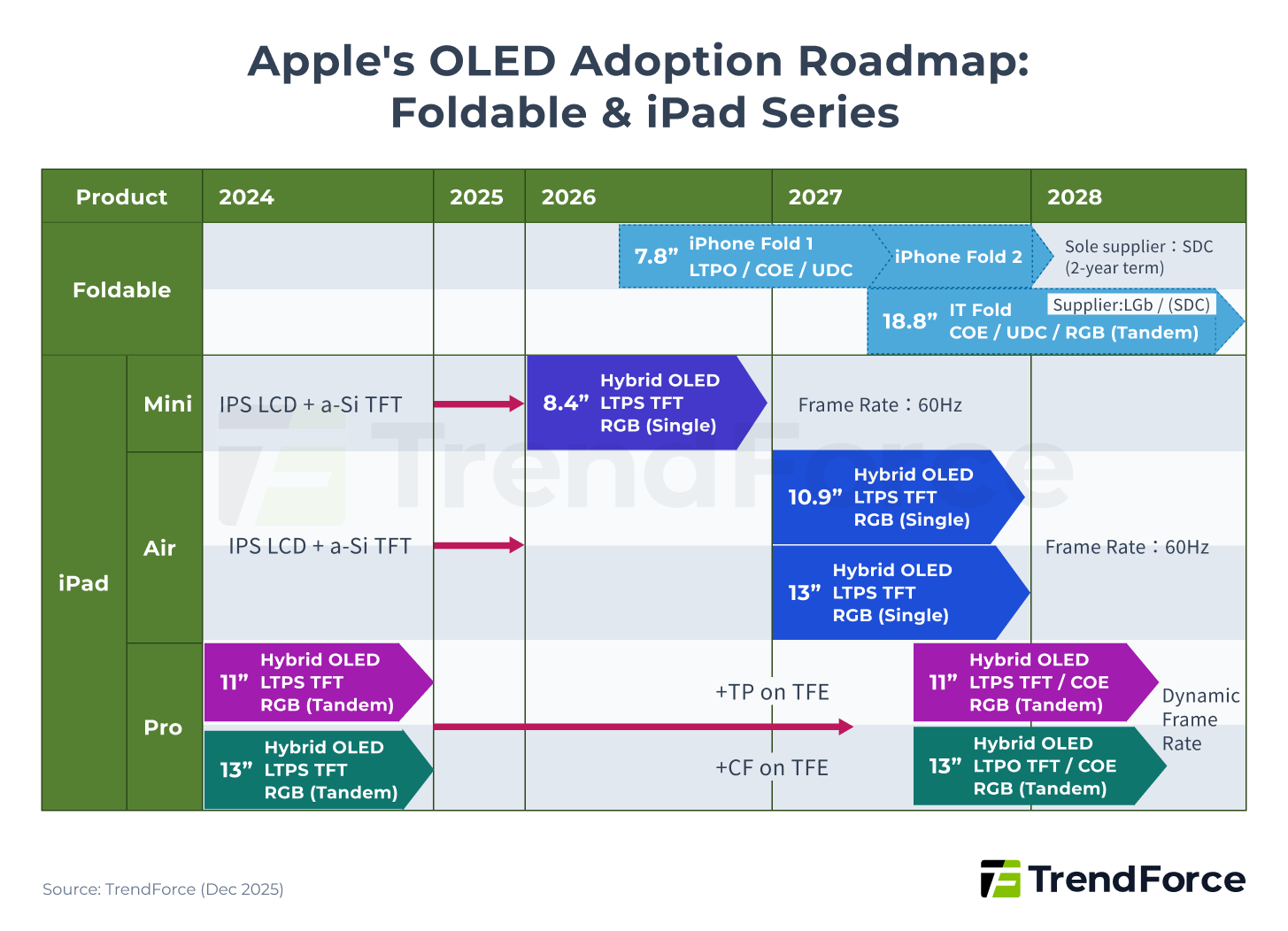

Because Apple’s specification upgrades and technological leaps invariably become the focal point of the supply chain, its official introduction of AMOLED panels to the iPad Pro series in 2024 once again captured the display industry's intense attention. Despite lukewarm sales in the first year of adoption, Apple’s resolve to expand its layout remains unshaken. Currently, Apple continues to map out a strategy to embrace AMOLED for its mid-sized product lines over the coming years while gradually phasing out the use of traditional LCD panels.

AMOLED Expansion: From iPhone to Foldables and IT Applications

Regarding its product roadmap, Apple has integrated AMOLED panels across its entire iPhone lineup, with the next milestone being the 2026 release of the Foldable iPhone. As Apple’s first foray into the foldable market, this launch is expected to inject significant new growth momentum into the sector.

For mid-sized products, beyond the existing adoption in the iPad Pro series, Apple plans to expand AMOLED technology to the iPad mini and iPad Air within the next two to three years.

Figure 2. Apple's OLED Adoption Roadmap: Foldable & iPad Series

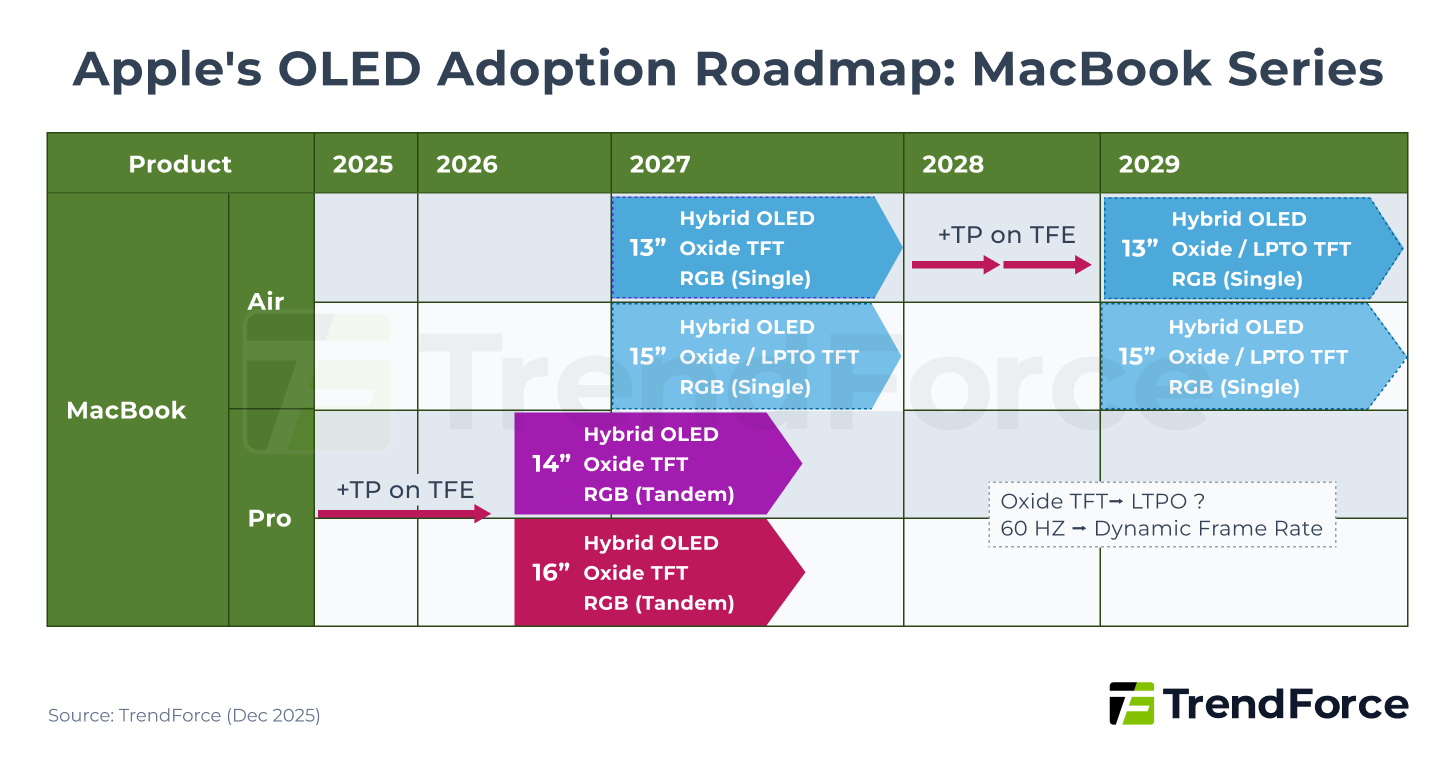

Regarding the MacBook lineup, Apple plans to incorporate AMOLED panels into the MacBook Pro series in 2026, officially entering the notebook market. Although originally slated for 2027, the AMOLED version of the MacBook Air is expected to be postponed to 2029 due to capacity allocation considerations and the pending sales performance of the initial Pro series. This suggests that by 2029–2030, Apple is likely to transition its entire mid-sized product lineup to AMOLED specifications.

Figure 3. Apple's OLED Adoption Roadmap: MacBook Series

The 16.2-inch and 14.2-inch display sizes of the MacBook Pro are significantly larger than those of the iPad Pro. To optimize production efficiency and capacity, Apple intends for MacBook AMOLED panels to be manufactured on Gen 8.6 lines, differentiating them from the existing Gen 6 production. This core requirement has ignited a surge in next-generation AMOLED investment. To secure Apple’s orders, major Chinese and Korean panel makers are aggressively deploying new capacity and advanced technologies.

AMOLED Set Shipment & Forecast - 4Q25

Tracking AMOLED end-product shipments across Smartphone, Notebook, Monitor, and TV sectors. Gain precise insights into brand performance, market penetration, and long-term growth forecasts.

Stay UpdatedChina-Korea Gen 8.6 AMOLED Production Race: Samsung Leads as China Closes the Gap

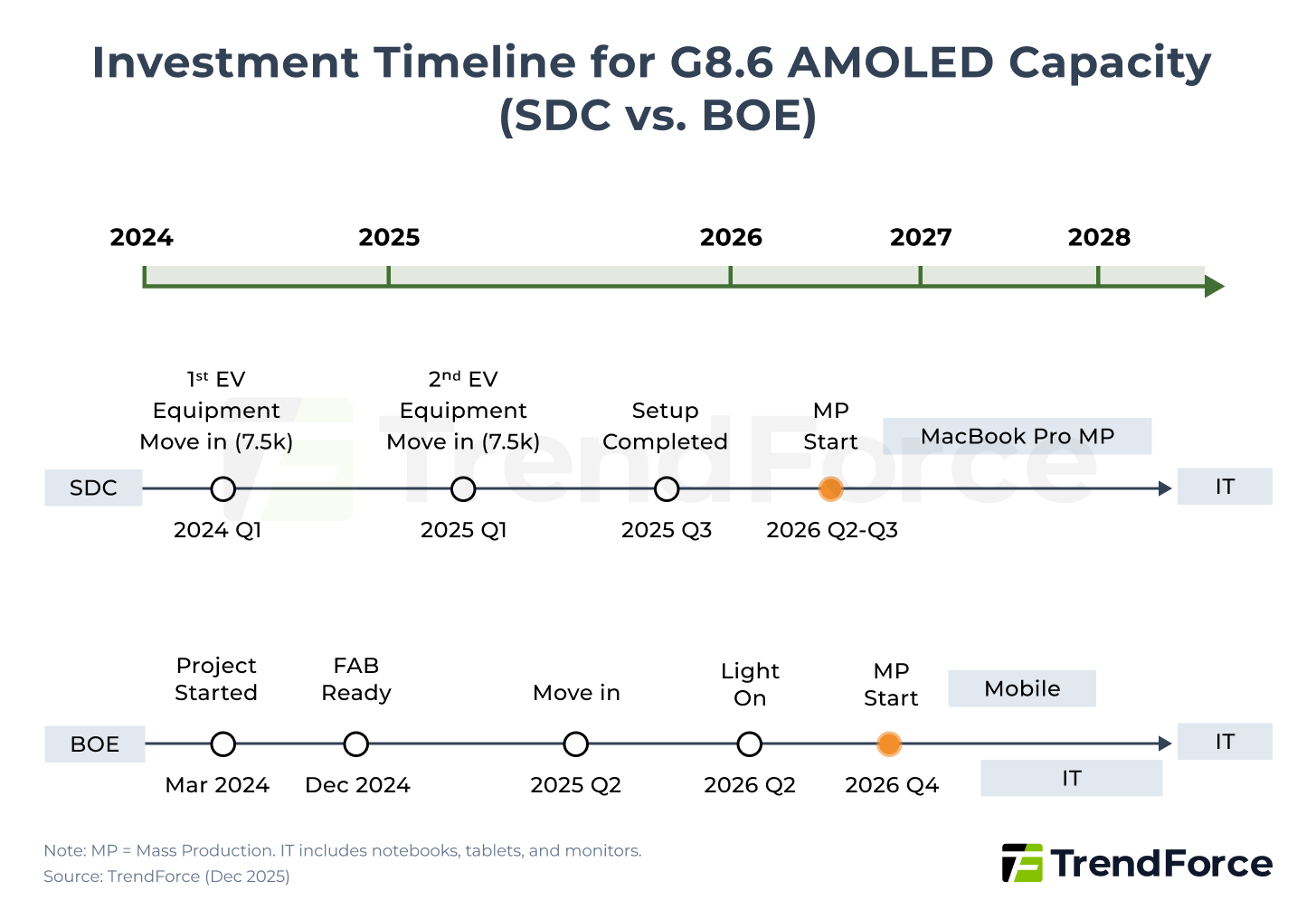

Regarding the current wave of large-generation AMOLED investment, Samsung Display (SDC) led the way in 2023 by announcing a 4 trillion KRW investment to construct a Gen 8.6 AMOLED production line, with mass production expected as early as the second quarter of 2026. As the sole current supplier of AMOLED panels for Apple’s MacBook Pro series, Samsung has already secured a strategic high ground.

Simultaneously, Chinese panel giant BOE followed suit at the end of 2023, announcing its own Gen 8.6 AMOLED investment, with mass production slated for the second half of 2026, reflecting its determination to bridge the technological and supply-side gap with its Korean rival.

Figure 4. Investment Timeline for G8.6 AMOLED Capacity (SDC vs. BOE)

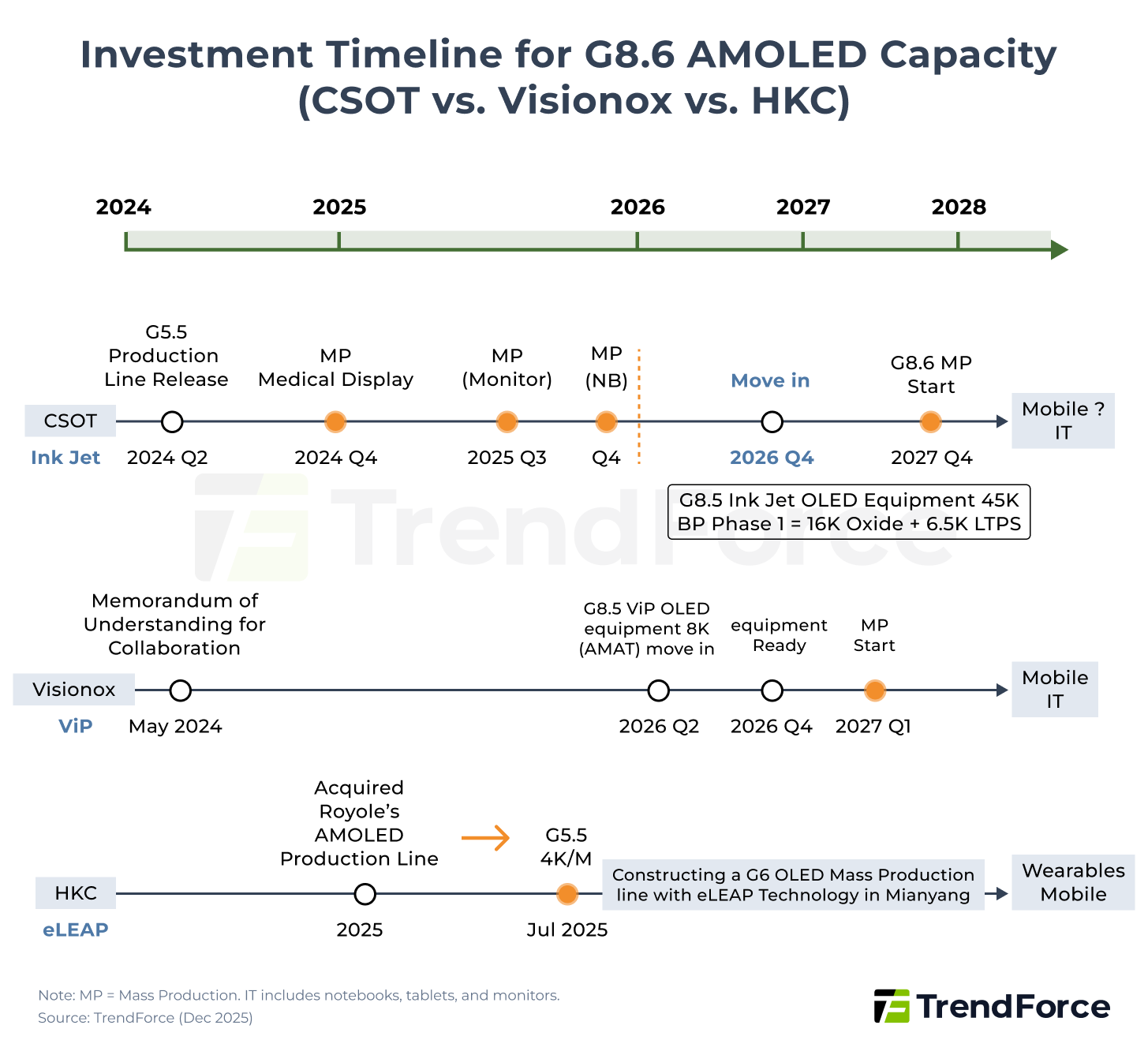

In Q2 2024, Visionox followed suit by announcing its investment in building a Gen 8.6 AMOLED production line. Unlike Samsung Display and BOE, which continue to focus on FMM (Fine Metal Mask) AMOLED technology, Visionox plans to use its ViP (Visionox intelligent Pixelization) technology, developed in collaboration with AMAT, to produce AMOLED panels via photolithography instead of FMM. This line is expected to start mass production as early as the first half of 2027.

Subsequently, CSOT officially announced the launch of its T8 project in Q4 2025, which will focus on an IJP OLED (Ink-jet printing OLED) technology-based Gen 8.6 production line. Mass production is anticipated to begin in the second half of 2027.

Meanwhile, HKC has accelerated its deployment in the AMOLED space. In addition to acquiring production lines from Royole, HKC has been in active discussions with JDI to collaborate and acquire its discontinued eLEAP technology, and may even consider investing in a new AMOLED production line in China in the future. These moves signify how Chinese panel makers seek to leapfrog competitors in the next-generation display battlefield through alternative technologies.

Figure 5. Investment Timeline for G8.6 AMOLED Capacity (CSOT vs. Visionox vs. HKC)

AMOLED Panel Shipment Tracker - 4Q25

Quarterly AMOLED shipment tracking: Covering TV, Monitor, Notebook, and Smartphone markets. Precisely quantify shipment performance by brand and by size on an annual and quarterly basis.

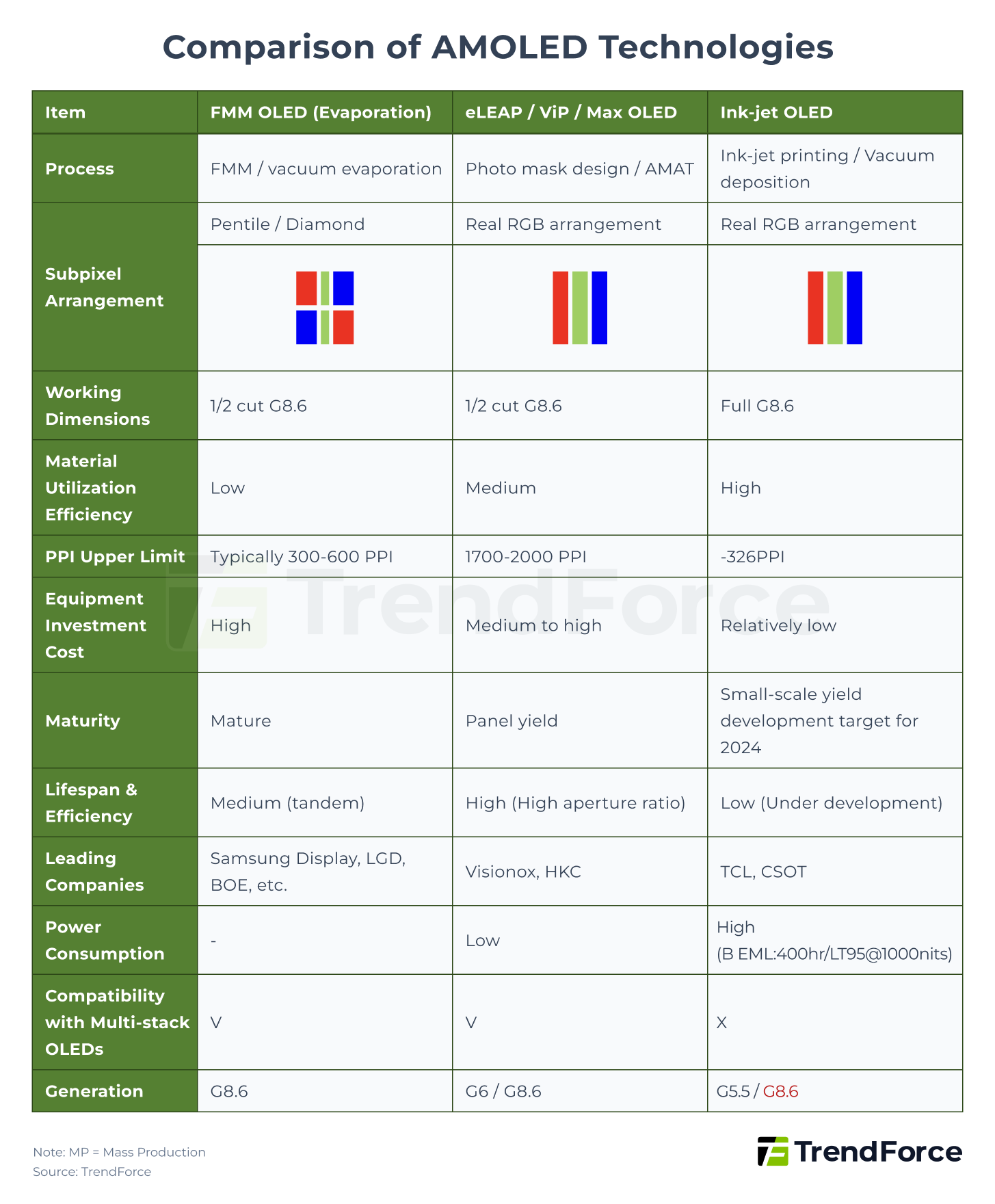

Stay UpdatedMature FMM Technology vs. Innovative Photolithography and Printing Technologies

The traditional FMM AMOLED technology, having been developed over a longer period, is relatively mature with a well-established supply chain for related equipment and materials. During the transition from Gen 6 to Gen 8.6, the primary challenge lies in addressing yield issues related to uniformity, which arise from the larger production area. With recent product applications shifting from smartphones to mid-sized panels, the advantages of conventional FMM AMOLED technology may give it a head start in meeting customer demands.

In comparison, the ViP technology, which eliminates the need for FMM and uses photolithography, holds theoretical advantages, such as enabling Real RGB pixel arrangements and achieving resolution specifications of over 1700 PPI. This makes ViP technology potentially suitable for panels of all sizes and applications. However, the main challenge lies in the production process, where the pixel layers must be selectively deposited and encapsulated one at a time, requiring multiple cycles of evaporation, photolithography, and encapsulation to complete the RGB pixels. Controlling and improving yield during these repeated processes remains a significant hurdle yet to be overcome.

Meanwhile, CSOT's IJP OLED technology has been under development for a considerable time and only recently progressed toward mass production. Through its printing process, IJP OLED technology can also achieve Real RGB pixel arrangements and, unlike traditional vapor deposition, it boasts significantly higher material utilization rates. This gives it a theoretical cost advantage. However, due to limitations in printhead capabilities and material molecular size, its current resolution is capped at around 350 PPI. Additionally, due to the characteristics of its solvent-based materials, there is still room for improvement in terms of product lifespan. At present, CSOT is the only panel maker globally that continues to invest heavily in IJP OLED technology. Substantial time and resources will still be required to fully develop a robust supply chain for its equipment and materials.

Based on observations, IJP OLED technology's specifications and current market dynamics suggest that its initial focus will likely be on the monitor market, serving as a stepping stone. Gradually, its adoption may expand to higher-PPI notebook markets. This also indicates that in the next two years, IJP OLED technology will directly compete in the monitor market against QD-OLED and WOLED technologies from the two major Korean panel makers.

Figure 6. Comparison of AMOLED Technologies

Cost Simulation and Analysis of AMOLED Technological Approaches

Among various technological approaches, costs vary significantly due to factors such as material utilization, product yield, and performance. For ViP technology, due to its initially low yield rate, the estimated cash cost of producing a 16-inch notebook panel could reach as high as USD 1,000 to USD 1,500 or more in the early stages. In comparison, the cash cost for Gen 8.6 FMM AMOLED during the same period is estimated to range between USD 300 and USD 400, resulting in a cost gap of approximately 3 to 4 times. Once the yield rate of ViP technology improves rapidly, the cost reduction will accelerate and could eventually approach the cost level of FMM OLED technology.

As for IJP OLED technology, its cost is influenced by material utilization, material performance, and yield. Compared to traditional FMM AMOLED technology, IJP OLED achieves higher material utilization, potentially saving about 20–30% on material costs. However, its material performance is currently lower than that of traditional FMM AMOLED, which may lead to yield losses. As a result of these offsetting factors, the estimated cash cost of producing a 16-inch notebook panel using IJP OLED technology may initially exceed that of Gen 8.6 FMM AMOLED. Nevertheless, as material performance continues to improve, there remains significant potential for cost optimization and reduction in the future.

AMOLED Technology and Market Status - 4Q25

Monitor penetration, market shares, maker strategies, and R&D evolution. Gain decisive insights into production layouts and cost dynamics across all applications.

Gain Insights2026–2030 Key Transformations in the Display Industry

Whether viewed from the supply side, characterized by the technological competition between Chinese and Korean panel makers, or the demand side, where AMOLED panels are transitioning from smartphones to mid-sized applications, both drivers have significantly fueled a new wave of large-generation AMOLED capacity investments over the past two years.

In this context, Chinese panel makers have demonstrated a particularly aggressive strategic offensive; of the four Gen 8.6 AMOLED production lines announced globally, three are located in China. These three major manufacturers are pursuing diverse technological strategies, with each betting on a different technical path. By exploring the viability of various technologies, Chinese firms aim to mitigate risks while seeking opportunities to leapfrog competitors and secure a first-mover advantage in the industry.

TrendForce observes that the future of mid-to-large-sized AMOLED technology and capacity may hinge on the following key developmental factors.

Rising Risks of AMOLED Overcapacity: Price Wars May Drive Market Penetration

Based on current capacity expansion plans, the maximum output of AMOLED notebook panels could reach 100 million units by 2035, accounting for 43% of the global annual notebook panel market volume of 230 million units. This implies that to accelerate capacity utilization and increase penetration rates, panel makers may adopt more aggressive pricing strategies to encourage the adoption of AMOLED notebook panels.

Whether panel makers can maintain high profit margins amidst heightened competition remains uncertain. Moreover, in the initial stages of mass production, due to a limited mid-sized client base, panel makers might consider reallocating capacity to other applications, such as the smartphone panel market, potentially intensifying competition in that sector.

Strategic Advantages of Chinese Manufacturers: Localization of the Supply Chain Yields Cost Dividends

From another perspective, China’s domestic AMOLED material supply chain has gradually matured over the past few years, driven by the expansion of Gen 6 capacity. Related companies are now aggressively setting their sights on Gen 8.6 components and materials. Since the price gap between overseas and domestic suppliers often reaches 20–30%, Chinese panel makers could progressively leverage significant cost advantages through increased localization. Based on cost models, if Chinese panel makers fully adopt domestically sourced components and materials, their material costs could be reduced by approximately 30%. According to this projection, the cash cost of producing a 16-inch AMOLED notebook panel using LTPO technology could approach that of panels using traditional Oxide TFT backplane technology, significantly enhancing cost competitiveness and supply chain autonomy.

Although the initial yield rate and specifications of Chinese panel makers may not yet match those of major Korean manufacturers, China benefits from its vast domestic market as a foundation and testing ground. China aims to replicate its successful model from the TV market; while it may currently lack powerful, large-scale brands, its low production costs serve as a key driver to bolster local OEMs and niche brands to refine the IT supply chain. Under this development model, whenever capacity needs to be absorbed, Chinese panel makers can rely on this domestic ecosystem to utilize excess capacity while simultaneously strengthening their local supply chain and expanding their influence.

Overall, after securing dominance in the LCD sector, Chinese panel makers are shifting their attention toward cutting-edge AMOLED technologies. By leveraging their past success in the LCD market, they aim to replicate that success in the AMOLED sector through aggressive pricing strategies and cost optimizations, gradually establishing dominance in this next-generation display battlefield.

Defensive Strategies of Korean Manufacturers: Counterattacking with Technical Moats and Specification Segmentation

For Korean panel makers, the competition in the AMOLED sector is a battle they cannot afford to lose. Faced with the aggressive expansion of Chinese manufacturers, their core strategy lies in leveraging deeper R&D expertise and yield control to lock in different product positionings through the segmentation of AMOLED specifications:

- High-End Market: Continuously raising technical benchmarks to maintain a lead in technological superiority.

- Mid-to-Low-End Market: Leveraging cost optimization and the depreciation advantages of existing production lines to provide customers with reasonable specifications and competitive pricing while maintaining profitability, thereby squeezing the profit margins of latecomers.

TrendForce concludes that whether Korean or Chinese, large-scale panel groups with more comprehensive resources will occupy a more advantageous position. These players are better equipped to handle the initial cost pressures associated with new AMOLED production capacity and new product launches during the early stages.