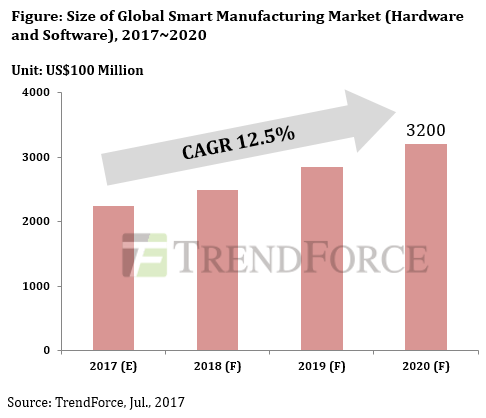

TrendForce Forecasts Size of Global Market for Smart Manufacturing Solutions to Top US$320 Billion by 2020; Product Development Favors Integrated Solutions

Industry 4.0 is a concept that has attracted a lot of attention in the global marketplace since its emergence in 2012. Following this conceptual framework, manufacturing companies in various industries have embarked on a mission to transform their operations by deploying smart technologies. TrendForce’s ongoing coverage of smart manufacturing solutions indicates that investments in related hard- and software have been growing steadily. Furthermore, this market is seeing rising demand and a trend towards integrated solutions. TrendForce forecasts that the size of the global market for smart manufacturing solutions will surpass US$320 billion by 2020.

Smart manufacturing is not simply about increasing the efficiency of the fabrication process. The concept also represents a paradigm shift in the operation and management of the manufacturing company. Upgrading software is therefore as important as upgrading the hardware. For instance, the deployment of edge computing – the processing of data near their origins (i.e. fabrication equipment) – optimizes data transmissions between the factory and the cloud platform that oversees the plant. This in turn raises the efficiency of hardware at both ends. Another example in the software area is artificial intelligence (AI). Effective AI and data analytics tools can parse through vast amounts of information uploaded from factories and find new ways to improve the fabrication process. In sum, the integration of hard- and software is crucial to the development of smart manufacturing solutions.

Numerous companies across IT and manufacturing supply chains have already entered the market for smart manufacturing solutions, including major global brands such as Intel, Xilinx and Microsoft. Active Taiwan-based market entrants include Advantech, HIWIN and ICP DAS. The diversity of solution providers again reflects the importance of hard- and software integration. As the number of vendors increases, TrendForce projects that the size of the global smart manufacturing market will grow at a CAGR of 12.5% from 2017 to 2020.

Customers demand integrated solutions because the design architecture of a smart manufacturing process is highly complex

For manufacturing companies, finding smart technologies that can address their specific needs has been a major challenge. Often, customers in the smart manufacturing market have to find different vendors to develop solutions for certain sections of their respective fabrication processes. Then, the customers have to combine the hard- and software that they have procured by themselves. Bringing these technologies together to create a tailored-made solution package is very difficult and can be costly. Thus, there has been some hesitation among manufacturers when it comes to investing in smart technologies.

TrendForce points out that companies such Siemens, GE and Schneider have recently launched their own unified Industrial Internet of Things (IIoT) platforms to meet the market demand for integrated solutions. There are also hardware vendors providing solutions that are highly compatible with different industrial hardware, software and cloud services.

For manufacturing companies, the goal of realizing smart manufacturing has been very difficult to achieve as there are hurdles in developing a unified design architecture and combining the various technologies. However, there has also been significant progress. Besides advances in hard- and software, networking standards for industrial applications have appeared (i.e. time-sensitive networking standards). Furthermore, the overall frameworks for IIoT, such as the Industrial Internet Reference Architecture (IIR) developed by the Industrial Internet Consortium (IIC), have matured during the past two to three years. The building of the infrastructure is now synergizing with innovations related to data applications, edge computing and cloud-based services (including the deployment of the hybrid cloud model). This in turn fosters a more stable, advantageous environment for developing solutions.

Going forward, vendors of cloud services will work their ways into the smart manufacturing market by offering solutions compatible with IT hardware for industrial applications. Correspondingly, hardware suppliers will first strengthen the foundation for smart manufacturing with more application-specific products that can better organize industrial data and connect to cloud-based platforms. Eventually, efforts from cloud service and hardware vendors will link up, and holistic solutions will emerge and provide manufacturers with unified platforms for managing their operations – the end goal for smart manufacturing.

TrendForce’s research also finds that manufacturing companies will adopt smart technologies and transform their operations gradually and in phases because of the complexities involved. They would have to make long-term, multi-year investments and commit millions or even tens of millions of dollars at every stage. Manufacturers therefore need to first identify the main challenges they need to overcome with the help smart technologies. Understanding their fundamentals will help companies gather the right data to use for revamping their fabrication processes as well as revolutionizing their business models.