Supplier Pricing Clash Crashes Prices to Reduce Inventory, NAND Flash Pricing Forecast to Drop by 15~20% in 4Q22, Says TrendForce

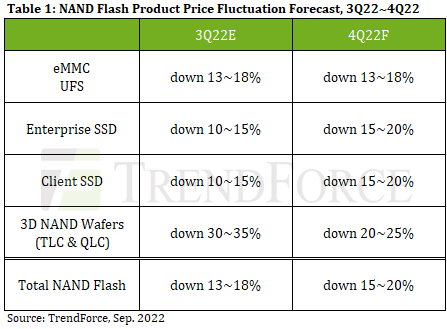

According to TrendForce research, NAND Flash is currently oversupplied. Buyers started focusing on destocking and greatly reducing purchases in 2H22 while sellers began offering rock-bottom prices to shore up purchase orders, causing wafer pricing to drop by 30-35% in 3Q22. All types of NAND Flash end products remain weak and factory inventory increased rapidly, resulting in a 15-20% decline in NAND Flash pricing in 4Q22. Most manufacturers’ NAND Flash product sales will also officially cross over into loss territory before the end of this year, which means that certain suppliers under pressure from operating at a loss will likely reduce production as a way to reduce losses.

In terms of client SSDs, since purchasing demand in 2H22 is far less than that in 1H22, PC brands currently feel pessimistic regarding demand next year and reducing inventory is a top priority, causing suppliers to increase client SSD price flexibility to surge shipments. PCIe 4.0 SSD shipments continued to rise this year and more suppliers launched 176-layer products to increase the penetration rate of this interface. In particular, 512GB quickly became the focus of supply. Coupled with a large supply of QLC SSDs, the supply side generally latched onto the 512GB capacity for fixed-volume or two quarter consolidated price negotiation strategies, intensifying price competition at this capacity. The decline in PC client SSD pricing is estimated to broaden to 15~20% in 4Q22.

In terms of Enterprise SSDs, purchase volume has also declined due to the expectation that server shipments will fall in 4Q22. However, though demand for consumer products has dropped significantly, manufacturers are eager to expand sales of enterprise SSDs. Notably, U.S. manufacturers began providing 176-layer products to clinch market share and Solidigm released a SK hynix 128-layer enterprise SSD for customer verification. At the same time, Kioxia is eagerly partnering with North American cloud service providers for PCIe 4.0 SSD. Price competition among suppliers is bound to intensify as more products enter the market. Thus, the price of enterprise SSD is forecast to drop by 15-20% in 4Q22.

In terms of eMMC, sluggish demand for chromebooks and TVs is cultivating a negative attitude among buyers towards eMMC stocking. As for demand visibility of networking products, visibility is optimistically expected to extend to the end of the year but, considering sluggish overall demand, only limited support for eMMC demand can be provided by networking products alone. With weak demand for consumer products and sustained growth in supply and output, inventory pressure forced manufacturers to offer low prices in 3Q22 for fixed-volume sales in 2H22 to stimulate buyers' willingness to buy. However, buyers’ order requirements generally trend towards small quantities across several batches. This will lead to a decline of eMMC pricing until the end of the year and eMMC prices are estimated to fall by approximately 13-18% in 4Q22.

In terms of UFS, the main application of UFS which is the smartphone market remains weak and traditional peak season sales has fallen short of past performance. Brands retain high inventory levels in both whole devices and components and their willingness to buy UFS has decreased. Therefore, manufacturers began looking for fixed-volume shipments starting in 3Q22, aggressively attracting transactions with branded companies though low prices and reaching supply agreements with certain Chinese brands in succession. However, since the market is generally pessimistic regarding demand next year, the status of manufacturer transactions has been poor and inventory pressure has not eased significantly. Therefore, manufacturers will continue to intensify price incentives to stimulate stocking momentum. UFS pricing in 4Q22 is estimated to drop by approximately 13~18%, with further slips a possibility.

In terms of NAND Flash wafers, even though some module makers have experienced slight pressure relief after several quarters of inventory adjustment, the overall market situation is still pessimistic, so attitudes towards stocking is extremely passive. Demand for products such as SSDs, memory cards, and drives at the retail end is stagnant as consumer products continue its slump and fail to become a force supporting wafer pricing. The supply side continues to increase wafer supply and a slowdown in the pace of process migration to higher layers has not been realized. Since a downward trend in pricing is inevitable, manufacturers are forced to accelerate process migration to optimize cost structure. In addition, manufacturers have been slashing prices since 3Q22, resulting in wafer contract pricing quickly approaching factories’ cash cost. TrendForce observes, against the framework of a perfectly competitive market for NAND Flash, suppliers intend to accelerate wafer price drops, and NAND Flash wafer pricing in 4Q22 is estimated to fall 20-25% QoQ.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email Ms. Latte Chung from the Sales Department at lattechung@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://insider.trendforce.com/