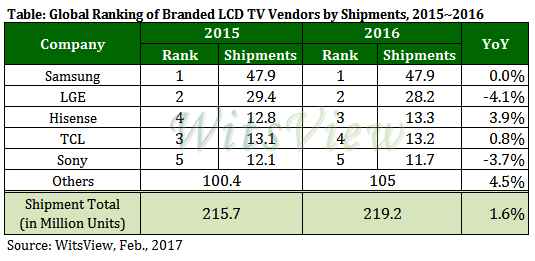

TrendForce Reports Global LCD TV Shipments Grew 1.6% Annually in 2016; Hisense Narrowly Beat TCL to Take Third Spot in Ranking

Global shipments of LCD TV sets for 2016 increased 1.6% annually to reach 219.2 million units, according to WitsView, a division of TrendForce. Shipment growth was attributed to the strong sales in North America’s distribution channels during the busy season, the increasing affordability of large-size TVs and the robust housing market in China. The top five TV brands by shipments in order are Samsung, LG Electronics (LGE), Hisense, TCL and Sony.

Samsung and LGE retained No. 1 and 2 in annual ranking

South Korea’s Samsung and LGE again took first and second in the annual ranking with 47.9 million and 28.2 million TV sets shipped, respectively.

“Samsung posted flat annual growth for 2016 as it experienced shortages for mid-size panels through the year,” said Ricky Lin, research manager of WitsView. Samsung’s TV set shipments were especially affected by the earthquake in southern Taiwan last February and issues that its in-house supplier Samsung Display (SDC) had with the adoption of Black Column Spacer (BCS) technology.

Lin added: “As Samsung and other TV brands competed for panel supply and switched to products belonging larger size segments, the average size of LCD TV sets also grew larger than originally anticipated for 2016.”

LGE registered a 4.1% annual decline in its shipments mainly because of the change in the brand’s strategic priority. After the reorganization of the group company at the beginning of 2016, LGE shifted its focus from expanding shipments to raising product margins and controlling its inventory level.

Hisense and TCL made gains by expanding into overseas markets

China’s Hisense and TCL took the third and fourth spot in the annual ranking by increasing their shipments 3.9% and 0.8% respectively, reaching 13.3 million and 13.2 million units. “Both brands relied on overseas markets to boost their shipments due to the gradual saturation of the domestic market,” said Lin. Competition in China will become more intense as Internet brands offer high-specification products at reduced prices to take market shares away from local second- and third-tier brands. With survival at stake, major domestic brands will grow even larger and push smaller competitors out of the market.

Sony ranked fifth in annual shipments with 11.7 million units, down 3.7% from 2015. Lin pointed out that large-size TV sets for the high-end segment will remain central to Sony’s strategy in 2017. “The Japanese brand is also going to introduce OLED TVs with advanced in-house video and audio technologies,” Lin also noted. “Sony has not featured OLED in its TV offerings since 2007. The latest OLED models are expected to spearhead a major campaign in the high-end market for the brand.”

Going into 2017, the market dynamics will be influenced by the closure of SDC’s L7-1 fab and Sharp’s decision to not use its Gen-10 plant to supply other first-tier brands. WitsView expects TV makers will increasingly focus on developing and promoting higher-margin products such as models featuring huge 4K displays. Consequently, the average size of TV sets will expand significantly as well.

WitsView’s latest analysis puts global LCD TV shipments for 2017 at 225 million units, an increase of 2.6% from 2016. Models sized 50-inch and larger will make up nearly 30% of total shipments for this year, while the share of UHD-resolution products in total shipments will reach 31.5%. The high-end segment will be a highly contest area for major brands. Samsung has recently launched its Quantum Dot (QD) TVs to compete against LGE’s OLED products. From the design perspective, bezel-less and detachable models are some of the novel concepts that the market can expect this year in addition to ultra slim models.