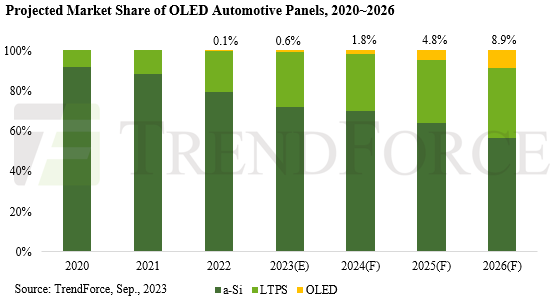

Market Share of OLED Automotive Panels Continues to Grow and Could Reach 10% by 2026, Says TrendForce

The latest “Automotive Display Market Analysis” from TrendForce indicates that the overall demand for automotive display panels (automotive panels) is gradually stabilizing and shows an upward trend as the automotive market as a whole slowly recovers, and promotional activities related to smart cockpits continue to expand. TrendForce estimates that the overall supply of automotive panels will maintain growth for 2023. Additionally, by 2026, TrendForce forecasts that the annual total supply of automotive panels will surpass 240 million pieces. Furthermore, as panel makers improve their OLED products in terms of performance and cost optimization, the market share of OLED in the market for automotive panels is forecasted to reach 8.9% by 2026.

The ongoing inflation has resulted in a significant decline in the demand for consumer electronics, prompting panel manufacturers to shift their focus towards automotive displays. Regarding the development of automotive panels, automobile manufacturers are now increasingly demanding greater integration in terms of design and functionality. This opens up new opportunities for panel makers to expand their presence downstream by offering system integration services. Panel makers aim to loosen the tight control that traditional Tier-1 automotive suppliers have over various automotive parts and components. Specifically, for displays used in cockpit systems, panel manufacturers are looking to establish a new kind of supply relationship with automobile manufacturers.

Automotive displays, including rear-seat entertainment screens, passenger-side displays, central information displays, and digital clusters, are evolving into more powerful communication mediums. Moreover, to integrate the various independent functions found in a traditional cockpit, larger screens and more flexible spatial designs are required. Hence, there is room for further advancements in various display technologies. For instance, pairing LCDs with a Mini LED backlight can significantly boost display brightness to over 1,000 nits, thereby improving display visibility when external conditions like snow and bright sunlight could cause interference. OLED panels, in contrast to traditional LCDs, offer notable advantages. They are self-emissive and thinner. They have a higher refresh rate and can be built on flexible substrates. These advantages can provide significant added value for automotive displays. Flexible OLED panels, in particular, allow for more innovations in vehicle design and are primarily positioned for flagship and high-end products in the automotive market.

In order to resolve the issue of durability for OLED among automotive applications, the technology is mostly adopted with Tandem OLED, which inter-concatenates and stacks multiple OLED components to form a high-efficiency OLED structure. Double-stacked OLED components require 1/2 less current density than that of single-layer variations after concatenation and are able to improve by a minimum of a twofold increase in lifespan under a much lower power consumption from panels. As for cost, Hybrid OLED panels are incorporated, where the assimilation between rigid OLED glass substrates and the thin-film packing technology used by flexible OLED would both reduce weight and cut cost, and curving effects can also be attained through thinned substrates.

TrendForce commented that a closer partnership between panel makers and automobile manufacturers is bound to be inevitable, should the former wish to expedite their market shares, seeing how automotive displays require approximately 2-3 years for testing and qualification. Subsequent to Samsung Display successively acquiring major orders from Ferrari and BMW, automotive leader LG Display has also announced to enhance its partnership with 9 luxury automotive brands by widening in incorporation of high-end automotive OLED panels, and is scheduled to mass produce its second generation Tandem OLED, which has been vastly improved in brightness and power consumption. While LCD adopted with Mini LED BLU (Mini LED backlight technology) races to seize the automotive market through cost advantages, OLED is accelerating its entry into the high-end automotive display market by launching ultra-large, rollable, and transparent products.

For more information on reports and market data from TrendForce’s Department of Display Research, please click here, or email Ms. Grace Li from the Sales Department at graceli@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://insider.trendforce.com/