Popular Keywords

- About Us

-

Research Report

Research Directory

Semiconductors

LED

Consumer Electronics

Emerging Technologies

- Membership

- Price Trends

- Press Center

- News

- Events

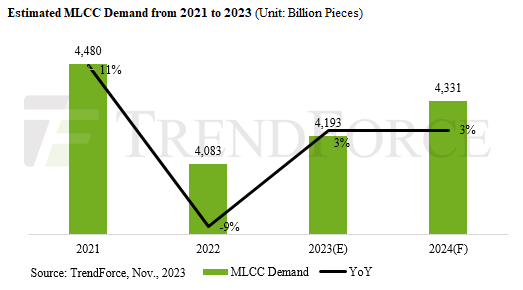

TrendForce reports that global demand for MLCCs is set to experience a period of slow growth from 2023 to 2024. With limited opportunities for industry growth, the demand for MLCCs in 2023 is estimated to be around 4.193 trillion units, with a modest annual growth rate of about 3%. This growth is primarily attributed to applications in smartphones, automotive electronics, and PCs. Given the uncertain political and economic climate, OEMs and ODMs have adopted a conservative outlook, with a slight increase of 3% in MLCC demand expected in 2024, reaching approximately 4.331 trillion pieces.

After accelerating their orders at the end of the third quarter, OEMs have become more cautious in stocking up for the fourth-quarter holiday season, resulting in a slowdown in orders for ODMs. Plans are underway to finalize pricing negotiations for 1Q24 by December 1st in preparation for the impending off-peak season. MLCC suppliers, facing lower-than-expected demand during the peak season and concerned over the potential continued impact of global economic weakness in 1H24, are focusing on strict control of production capacity and inventory levels.

Demand for smartphones, PCs, and notebooks is gradually improving from its previous low, but overall consumer confidence remains weak

Benefiting from a slight stabilization in PC/notebook demand in the third quarter, MLCC shipments in September reached a peak of approximately 434 billion units. The launch of new smartphone models in the fourth quarter has led to an increase in shipments of related components, including PA modules and WiFi/5G chips from suppliers like AWSC and MediaTek, with a shipment volume of 410 billion units in October and an average BB ration of 0.94.

However, recovery in industry confidence still lacks solid support from broader social and economic stability, leading to a slow increase in overall consumer demand. MLCC demand in November is expected to decrease to 405 billion units, with the BB ratio dropping to 0.92.

Industry demand stabilizes as suppliers boost production capacity, and Japanese suppliers Murata and Taiyo Yuden compete aggressively for orders

In response to strategic adjustments, Murata and Taiyo Yuden showcased impressive performances in their third-quarter financial reports. Benefiting from increased operational capacity and a shift from loss to profit, as well as bolstered by Japan’s relaxed monetary policy, both companies experienced growth in revenue and profits. Notably, Murata’s operating profit margin surged significantly, recording a 77.2% increase for the quarter. Following a year of conservative pricing and financial stabilization, along with signals of a rebound across various industries. Murata is planning aggressive pricing strategies starting from 1Q24, focusing on high-capacity, high-temperature, and high-pressure resistant products to strategically position itself as it battles it out for order acquisitions in 2024.

Samsung and Yageo have also significantly reduced the prices of their high-end MLCC products, ranging from 10u to 47u X5R–X6S, with an average quarterly price reduction of about 3–5%. Therefore, TrendForce believes under the expectation of slow growth in the MLCC industry, suppliers’ breadth of product applications and the financial resilience of their operations will be critically tested in 2024.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email the Sales Department at SR_MI@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit https://www.trendforce.com/news/

Subject

Related Articles

Related Reports