Popular Keywords

- About Us

-

Research Report

Research Directory

Semiconductors

LED

Consumer Electronics

Emerging Technologies

- Membership

- Price Trends

- Press Center

- News

- Events

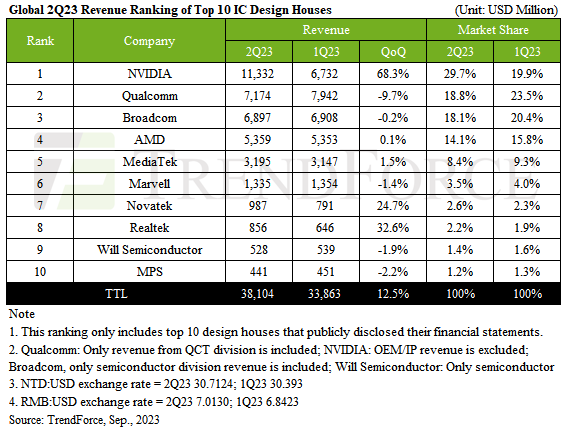

Fueled by an AI-driven inventory stocking frenzy across the supply chain, TrendForce reveals that Q2 revenue for the top 10 global IC design powerhouses soared to US $38.1 billion, marking a 12.5% quarterly increase. In this rising tide, NVIDIA seized the crown, officially dethroning Qualcomm as the world's premier IC design house, while the remainder of the leaderboard remained stable.

AI charges ahead, buoying IC design performance amid a seasonal stocking slump

NVIDIA is reaping the rewards of a global transformation. Bolstered by the global demand from CSPs, internet behemoths, and enterprises diving into generative AI and large language models, NVIDIA's data center revenue skyrocketed by a whopping 105%. A deluge of shipments, including the likes of their advanced Hopper and Ampere architecture HGX systems and the high-performing InfinBand, played a pivotal role. Beyond that, both gaming and professional visualization sectors thrived under the allure of fresh product launches. Clocking a Q2 revenue of US$11.33 billion (a 68.3% surge), NVIDIA has vaulted over both Qualcomm and Broadcom to seize the IC design throne.

Qualcomm's Q2 took a hit as the Android smartphone sector grappled with dwindling demand and Apple's modem pre-purchases resulted in a subdued seasonal rhythm. Consequently, their revenue slid by 9.7%, rounding off at about US$7.17 billion. Broadcom, while benefiting from AI-ignited demand for high-end switches and routers, faced headwinds with revenue drops in server storage, broadband, and wireless. The result was a second-quarter revenue that essentially mirrored the previous quarter at around US$6.9 billion.

AMD's Q2 performance plateaued at about $5.36 billion, weighed down by a slump in gaming GPU sales and its embedded segment operations. Conversely, MediaTek, after several quarters of inventory recalibration, witnessed a resurgence with components like TV SoCs and Wi-Fi stabilizing. The added impetus of urgent TV orders and escalating shipments for mobile phones, smart platforms, and power management ICs boosted MediaTek's Q2 to a solid US$3.2 billion.

Marvell, though buoyed by AI deployments in data centers, faced headwinds with a decline in On-Premise Servers (enterprise private clouds). End-user demand remained frail, and with sectors like data centers, telecom infrastructure, and enterprise networking facing revenue drops, Marvell's Q2 took a 1.4% hit, culminating at roughly $1.33 billion.

Taiwan's IC design stalwart Novatek flourished as customers replenished TV-related inventories and ushered in novel products such as OLED DDI. Realtek, drawing strength from supply chain restocking of PC/NB-centric ICs, reported quarterly growths of 24.7% and 32.6%, respectively. Yet, without substantial signs of a holistic revival in end-sales and inventory restocking, growth in H2 seems set to face challenges.

Will Semiconductor secured the ninth spot with a Q2 revenue of $528 million, registering a modest decline of about 1.9%. Hot on its heels is the US-based power IC maestro, MPS, with its Q2 revenue tallying up to $441 million—a slip of approximately 2.2%.

Peering into Q3, while inventory levels across companies paint a rosier picture than H1, a pervasive end-user demand slump urges caution. However, a silver lining emerges with CSPs, internet titans, and private firms flocking to generative AI and large language models. As these high-value AI offerings gain traction, TrendForce projects that the top ten global IC design giants will continue their double-digit ascent in Q3, potentially reaching record-breaking figures.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email Ms. Latte Chung from the Sales Department at lattechung@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://insider.trendforce.com/

Subject

Related Articles

Related Reports