Popular Keywords

- About Us

-

Research Report

Research Directory

Semiconductors

LED

Consumer Electronics

Emerging Technologies

- Membership

- Price Trends

- Press Center

- News

- Events

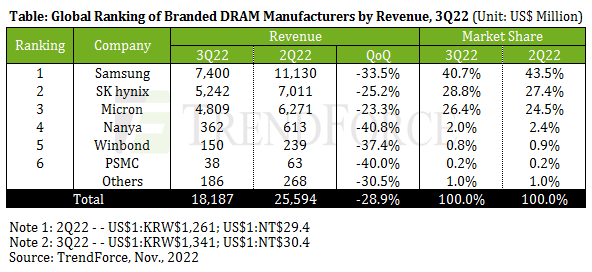

Global market intelligence firm TrendForce reports that for 3Q22, the revenue of the whole DRAM industry dropped by 28.9% QoQ to US$18.19 billion. This decline is the second largest to the one that the industry experienced in 2008, when the global economy was rocked by a major financial crisis. Regarding the state of the DRAM market in 3Q22, the QoQ decline in contract prices widened to the range of 10~15% as the demand for consumer electronics continued to shrink. Server DRAM shipments, which had been on a relatively stable trend compared with shipments of other types of DRAM products, also slowed down noticeably from the previous quarter as buyers began adjusting their inventory levels.

Turning to individual DRAM suppliers’ performances in 3Q22, the top three suppliers (i.e., Samsung, SK hynix, and Micron) all exhibited a QoQ drop in revenue. Samsung posted US$7.40 billion and a QoQ drop of 33.5%, which was the largest among the top three. SK hynix’s revenue fell by 25.2% QoQ to around US$5.24 billion. As for Micron, its revenue came to around US$4.81 billion. Since Micron marks its fiscal quarters differently, its DRAM ASP showed a QoQ decline that was smaller than the ones suffered by the two Korean suppliers. And as a result of this, Micron’s QoQ revenue decline was also the smallest among the top three. TrendForce points out that the top three are still maintaining a relatively high operating margin at this moment. Nevertheless, the inventory correction period that has started this year will last through the first half of next year, so they will experience a continuing squeeze on profit.

On the topic of suppliers’ capacity expansion plans, Samsung has gradually slowed down the transfer of its legacy wafer processing capacity from DRAM to CMOS image sensors due to the recent fall in demand for camera modules. Next year, Samsung will raise its DRAM production capacity as its new fab P3L enters operation. However, seeing that inventory reduction is not progressing at the originally anticipated pace, Samsung will decelerate its technology migration to limit its output growth. Looking at SK hynix, it will also rein in its output growth next year by putting some brake on its technology migration. Moving to Micron, it has pushed back the schedule for mass production with its 1beta nm process. This deferment has to do with the higher difficulty level for the development of this technology and the general demand slump. Micron’s output growth in 2023 is forecasted to be the smallest among the top three. Furthermore, TrendForce is not ruling out the possibility of Micron making more tangible production cuts in response to the rapidly shrinking profit margin.

With regard to Taiwan-based DRAM suppliers, Nanya suffered the largest QoQ revenue drop among the top six suppliers in 3Q22, reaching as much as 40.8%. Nanya’s result was attributed to the sizable share of consumer DRAM in its product mix as well as the sizable share of customers from Mainland China in its client base. Moving into this fourth quarter, Nanya has already scaled back wafer input but maintains the pace of its migration to the 1A nm. However, this technology will still be at the customer sample stage in 2023 as Nanya’s clients hold a cautious demand outlook and are thus not keen on adopting the more advanced process. Therefore, the 1A nm process is not expected to make a noticeable contribution to Nanya’s output until 2024. Turning to PSMC, its revenue fell by around 40.0% QoQ for 3Q22 owing to the plummeting consumer DRAM prices. PSMC’s DRAM revenue that is presented here mainly pertains to the sales of its branded DRAM products that are manufactured in-house and excludes its DRAM foundry service. However, if DRAM foundry service is included in the calculation, then the QoQ decline was 22.9%. Lastly, looking at Winbond, its 3Q22 revenue still showed a significant QoQ decline of 37.4% even with a fairly conservative pricing strategy. This has to do with the considerable contraction of its shipments. Winbond already lowered the capacity utilization rate of its fab in Taichung in 3Q22. As for the setup of its new fab in Kaohsiung, the schedule for entering the mass production phase has been pushed back slightly due to the unfavorable market situation. The Kaohsiung fab will initially manufacture DRAM using the 25S nm process. This is expected to be followed by the deployment of the supplier’s 20nm process in 2H23.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email Ms. Latte Chung from the Sales Department at lattechung@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://insider.trendforce.com/

Subject

Related Articles

Related Reports